Why Platinum Prices Have Fallen?

Four Reasons

A Short Term Phenomenon Allowing Exceptional Investment Opportunity

By David Mitchell

17th September 2021

Disclaimer : The information contained in this article should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. This article is our opinion and analysis.

Considering the long-term investment picture for Platinum is exceptionally supportive, with price forecasts based on serious long-term supply issues alongside rising demand curves, why on earth has Platinum fallen in price recently? Indeed why has the entire Platinum Group Metals (PGM) complex fallen since February / March 2021.

The fall in PGM prices has been driven by 4 major (short term) developments. A crystal ball would have been required to predict these exogenous shocks which we strongly believe to be short term in nature. As such, this presents an incredible buying opportunity at these depressed prices; prices that are not aligned with the overriding macro developments in this space.

1) ACP Processing Plants

South African Platinum output jumped (+644koz) year-on-year (following very depressed production numbers in the previous year) due to a return to full operations at Anglo American Platinum’s Converter Plant (ACP) in the beginning of 2021. This followed on from the complete shutdown at the beginning of Q2, 2020, as a result of an explosion.

Platinum supply was boosted over and above our original forecasted numbers by a faster-than-anticipated processing of a backlog of material that built up while ACP plants were out of action last year. The plants have been running at approximately 130% of machine capacity to process this ore grade as quickly as possible to raise cash critically required by the miners for extreme liquidity purposes.

This is a short term phenomenon as the stock piles have been rapidly dissipated without new ore production matching the processing rates of ore-grades. This has given the artificial impression of an abundance of metal coming onto market at a time of very depressed industrial usage.

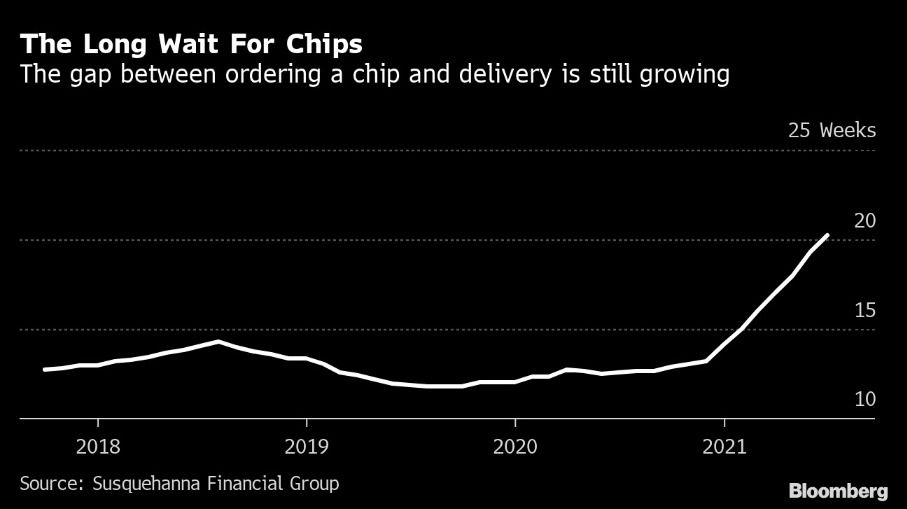

2) Chip Shortages and the Global Record Low Inventory of Unsold Car Stocks.

A chip shortage is a fairly rare occurrence in the semiconductor and integrated circuit industry. There is however currently, a substantial supply-deficit of chips that began to appear in January 2021. A surge of Covid-19 cases in Malaysia, a little-known but critical link in the semiconductor supply chain, has opened a new front in the battle to fix manufacturing woes that have rippled across industries during a global shortage of computing chips. Malaysia is one of the world’s top destinations for assembly and testing of the devices that control smartphones, car engines and medical equipment. Complete lockdowns occurred across the country in Q2, 2021 and had a major impact on chip manufacturers in particular. Malaysia accounts for over 13% of the global chip assembly testing and packaging.

Major repercussions have impacted automakers including Toyota Motor Corp., General Motors Co., Volkswagen AG and Ford to name a few and forced them to curtail car production quite dramatically as a result of the shortfall in chips. At the beginning of September, Toyota has yet again trimmed its annual production forecasts due to the constraint caused by Covid-19 and the effects on chip manufacturing.

A major worldwide auto inventory re-build is desperately overdue, with reported global inventories of unsold car stock at just one third of pre-pandemic and more importantly longer term historic levels. In the USA, this translates into less than a month’s supply of available inventory [Wards Intelligence]. We have seen this tightness globally with second-hand car market prices exploding higher in price around the world.

This inventory re-build of manufactured vehicles will quickly translate into an unprecedented demand for Platinum Group Metals and in particular, Platinum itself.

3) Capitulation of Stock Inventory Held by Car Manufacturers

Car companies generally have a poor reputation within the industry when it comes to timing their inventory stock accumulation and selling down their stock held. The larger conglomerates have established advanced trading rooms within their global companies to help accommodate volatility in commodity pricing and somewhat utilising hedging strategies to mitigate this risk. These trading rooms seem to lack price sensitivity with regards to Platinum Group Metals and do not seem to actively analyse long-term price analysis or account for major commodity trends.

They have a reputation for stockpiling at the highs and capitulating stock towards the cyclical lows. End user manufacturers have direct contracts for the offtake of refined material from the producers, especially when it comes to Palladium for example. Over the last few years, demand for the metal has considerably outpaced their offtake supply contracts.

This forced global slowdown of car manufacturing as a direct result of chip shortages, has forced car conglomerates into continued stockpiles as a function of their pre-existing buying contracts, at a time when usage is essentially falling. With falling prices and the lack of complete hedging strategies, car conglomerates have been forced to offload their surplus inventory into the market, as a result of acute capital losses. We have seen this price action very clearly with Rhodium falling from the March highs of just shy of US$30,000 to sub US$10,000 this week, and also the recent palladium falls in particular.

Car manufacturers have been reducing their stockpiles at probably the very worst time, hence the recent and severe price decreases in both Rhodium and Palladium.

4) Financial Traders / Banks Positioning in Platinum

Financial institutions that are seen to be at the coalface of recognising short term supply-demand curves, have taken advantage of the situation highlighted in Points 1 -3 above. With clearly definable technical support levels indicated on the Platinum price chart, financial institutions have instigated major short positions in Platinum, thereby fuelling the added pressure on falling prices.

According to recently released Commitments of Traders (CFTC) data, the spike in short positions (speculative short positioning has hit a 2 year high) has been obvious, but the managed money long positions have similarly hit their lowest levels in 12 years (since 2009!).

This is purely a speculative trade for the financial institutions for which, in time, they will not only need to buy back their short positions (short-covering) but will also have to instigate long positions to re-invest in Platinum for forward looking price appreciation.

We are also experiencing backwardation curves in the Platinum price, indicating pressures on short-term supply versus longer dated supply. From the March 2020 price lows in Platinum to the highs achieved in February 2021, we can equate important technical Fibonacci retracement levels. The first being the 50% retracement which equates to US$950 per Toz. The more important level is the 61.8% retracement in price which is US$859.00 per Toz.

With the backwardation in platinum prices on the long end of the curve has allowed them to initially start buying their platinum shorts back at discounted prices with delivery 3 to 4 months forward.

These financial institutions are extremely aware of these levels and are reputedly layering their buying orders from US$900 down to US$870 in order to accumulate as much as possible.

In Conclusion:

As PGM investors, we must focus our attention on the following metrics:

— Supply and Demand

— The progressive tightening of environmental regulations and technology innovation surrounding the production of green hydrogen which is actively leading towards a dramatic increase in PGM demand. Coupled with the existing supply-side constraints, caused mainly by the decline in South African mine supply (representing 73% of the world’s Platinum output) and the looming energy crisis caused South Africa’s national electricity public utility Eskom; this will almost certainly result in a major price resolution higher in Platinum

— Investment demand will likely be bolstered by the current low Platinum price in the context of a very positive fundamental outlook moving forwards.

It’s allowing us an incredible investment opportunity.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery across the world.

Consider the safest option of segregated, allocated vault storage at Le Freeport Singapore with Indigo Precious Metals.

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.