The global price revaluation occurring across precious metals is, in my view, relatively easy to understand when viewed through the real-world lens of monetary debasement, debt expansion and structures , unfunded liabilities, supply constraints, and the broader macroeconomic cycle.

However, what interests me most, and where we have demonstrated considerable success over the last few decades, is identifying severe pricing anomalies within the precious metals asset class. These anomalies can offer the potential for exceptionally high returns when they do finally correct.

It is important to remember that these pricing anomalies can remain suppressed or misunderstood for a long time. Markets can stay dislocated far longer than most investors expect. But once the pressure finally releases, the price adjustment can be extremely powerful and very quick, as the asset begins to rebalance toward its true macro fair value and underlying global supply-demand reality.

That is the area we focus on: recognising where the market has materially mispriced an asset, understanding why that mispricing exists, and positioning before the broader market finally wakes up to it.

In my view, the technical picture for platinum is not just constructive — it is exceptionally compelling.

To put this into historical perspective, silver delivered an extraordinary move during the 1970s, ultimately rising by roughly 44 times from its lows into the 1980 peak. During that move, the Gold-Silver Ratio compressed to around 17-to-1.

Today, that same ratio still sits around 62-to-1, which tells you one very important thing: there remains significant room for further relative repricing within the precious metals complex.

To be clear, in the bigger picture, whatever upside gold delivers during this revaluation cycle, we do expect silver to outperform gold by at least double in percentage terms. That has been our long-standing view, and the historical ratios, macro-fundamentals, exchange inventories and industrial complex demands strongly support that argument.

However, what is even more interesting today is what this tells us about platinum.

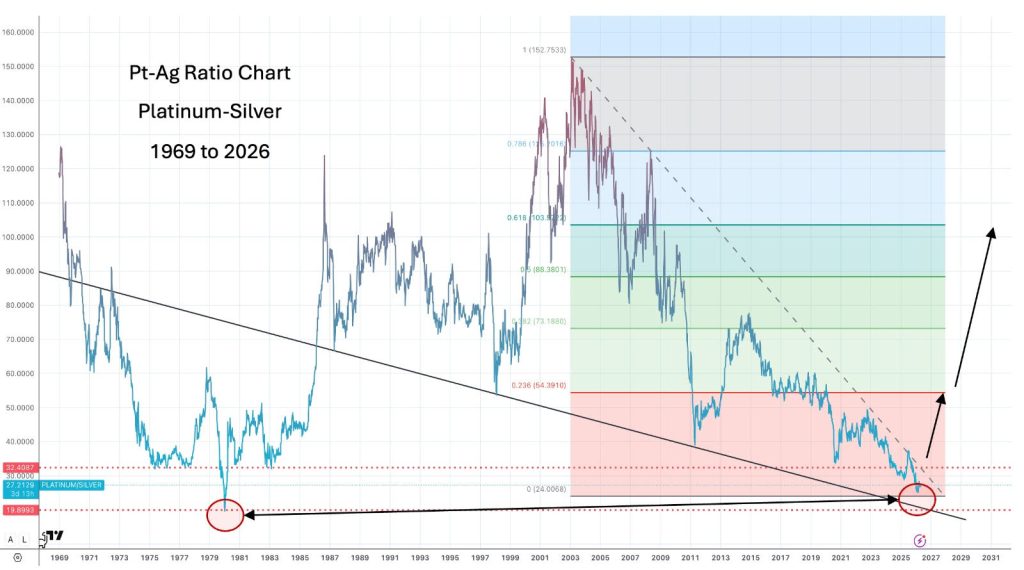

The silver blow-off into 1980 also drove the Platinum-Silver Ratio down to an all-time historical low of approximately 19-to-1. From that extreme undervaluation, platinum then went on to revalue dramatically, eventually reaching a ratio of around 154-to-1 versus silver.

That was an almost 8-fold relative price performance.

More recently, we have again traded back down towards that historic extreme, touching approximately 22-to-1. In my opinion, that represents an extraordinary undervaluation of platinum relative to silver and places the market very close to one of the most extreme relative valuation points ever recorded.

This is not a normal valuation structure.

As the chart below demonstrates, platinum has also formed a large multi-decade bullish pennant pattern. These are not the types of technical formations one normally sees at the end of a move. They are more commonly seen ahead of a major breakout and revaluation phase.

The Platinum-Gold Ratio tells an equally extraordinary story.

In 2025, platinum fell to approximately 0.27-to-1 versus gold, the lowest level in recorded pricing history since platinum was first recognised as a unique and distinct metal in the late eighteenth century.

Put simply, that is an historic anomaly.

For perspective, the Platinum-Gold Ratio has traded above 5.5-to-1 on several occasions, while the average over the last 50 years has been approximately 1.5-to-1. Historically, platinum has frequently traded at a premium to gold, and for long periods it was considered normal for platinum to command a higher price.

Today, platinum is priced at only around 40% of gold’s price.

That is an extraordinary dislocation.

Returning to the Platinum-Silver Ratio, even a modest recovery to the lower 23.6% Fibonacci retracement level would imply a move back towards approximately 54-to-1. That alone would represent more than a doubling in the ratio from current levels.

And that is before factoring in the very real possibility that silver itself moves materially higher during this cycle.

So what are we left with?

We are looking at a metal that is not simply out of favour, but deeply neglected.

We are looking at a market already in a structural supply-demand deficit.

We are looking at a price level that, by almost any historical comparison, sits at an extreme undervaluation.

And we are looking at a technical chart structure that strongly suggests platinum is building towards a major revaluation phase.

The fundamental backdrop is equally important:

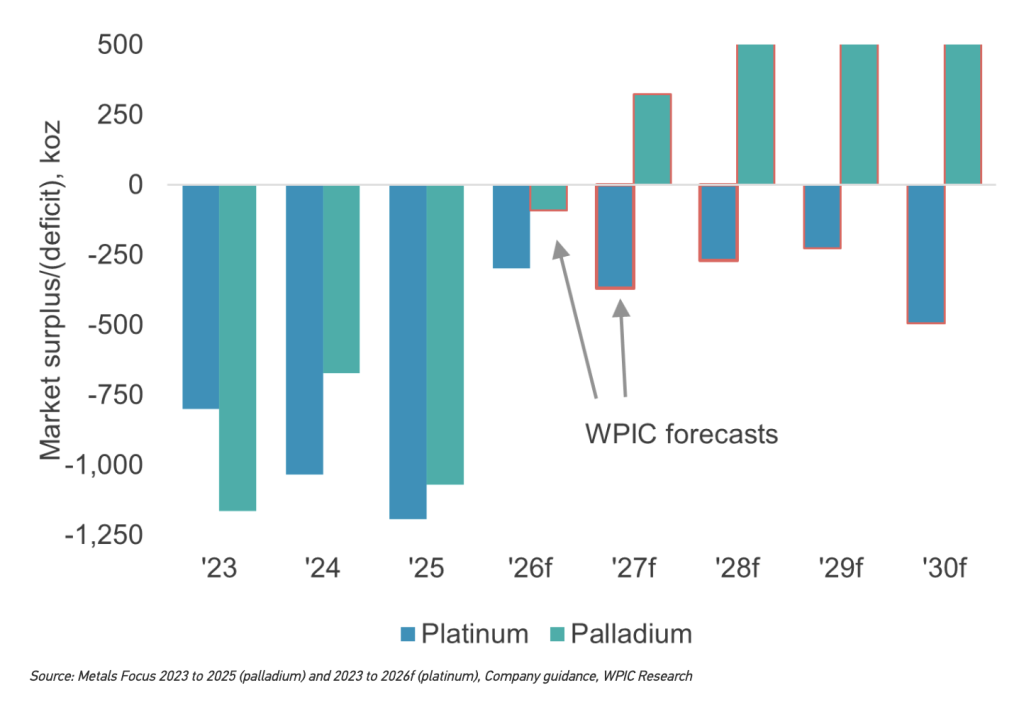

1. Persistent structural deficits

Platinum supply has fallen short of demand every year since 2023, and this deficit is expected to continue through to 2030.

2. Depleted above-ground stocks

A substantial annual surplus would be required to rebuild above-ground inventories back to sustainable levels. Until that happens, the market is likely to remain very tight.

3. Limited supply response

Platinum mine supply remains heavily constrained, with very limited ability to increase production in the short to medium term. Higher prices may eventually encourage additional recycling supply, but so far the response has been well below expectations.

4. Diverse and resilient demand base

Platinum benefits from a broad range of end uses, including automotive, industrial, jewellery, investment, hydrogen, and energy-related applications. Importantly, there are very few lower-priced alternatives that can easily replace platinum in many of these applications.

5. Extreme relative undervaluation versus gold

Despite all of this, platinum still trades at a massive discount to gold. Historically, that is highly unusual. In my view, it is also highly unsustainable.

The conclusion is simple.

Platinum is one of the most undervalued major precious metals in the market today, yes alongside silver. It combines an extreme technical setup, a deeply depressed relative valuation, persistent supply deficits, declining above-ground availability, and a price that remains substantially below gold.

That is not normal.

And in my view, it is unlikely to remain that way for long.

Disclaimer: This commentary is provided for informational purposes only and does not constitute financial advice or a solicitation to buy or sell any investment products. While every effort has been made to ensure accuracy, Indigo Precious Metals Group and Auctus Metal Portfolios accept no liability for any losses arising from reliance on the information contained herein. Clients should seek independent professional advice before making any investment decisions.