That is the mistake most analysts are making.

Everyone keeps dragging out the same historical comparison, 1971 to 1980, the great gold bull market, 27x performance, but they are missing the one violent variable that makes this cycle potentially far more powerful.

Central banks have changed sides.

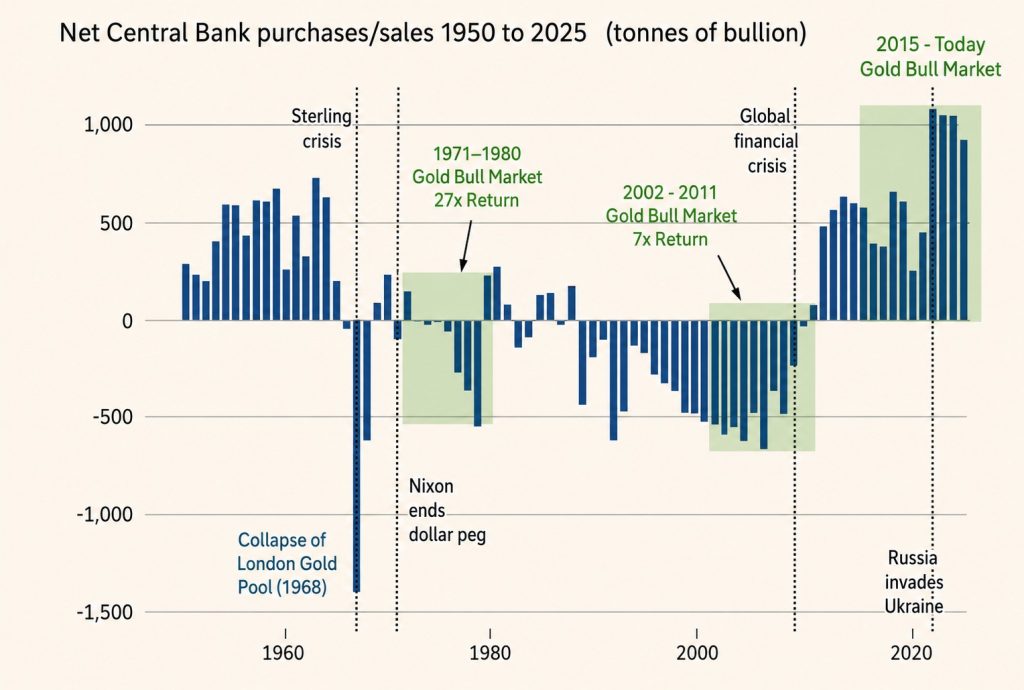

For decades, central banks were one of the great structural headwinds for gold. They were the sellers. They were the overhang or anchor dragging on prices. They were the institutions quietly feeding physical metal into the market and suppressing the very asset they now appear desperate to accumulate.

• In the 1970s, central banks were net sellers of over 1,000 tonnes.

• In the 2000s, they were net sellers of over 3,500 tonnes.

Now that script has flipped completely.

Central banks are no longer quietly signalling confidence in the fiat paper system. They are doing the opposite. They are diversifying their national balance sheets away from paper promises and into physical gold.

Read that again.

The very institutions responsible for managing the monetary reserves of entire nations are now buying gold in size. Not because it pays a yield. Not because it produces cash flow. But because, at the sovereign level, gold remains the one monetary asset with no counterparty risk.

That is not a footnote. That is the engine of this cycle.

Note: This new cycle, which began around December 2015 / January 2016 , has not been driven by wealth managers, pension funds or domestic investor demand. They have been marginal participants at best.

This cycle has been driven by something far more important: the very institutions that sit at the heart of the paper monetary system itself.

Central banks are no longer the anchor holding gold back.

They are the engine behind this cycle.

The great monetary rebalancing is not coming.

It is already here and more importantly ongoing.

And when the paper system begins to wobble under the weight of its own extreme debt and extreme leverage, history is very clear on what eventually wins:

Physics and atoms ‘over’ paper derivatives.

Particularly when the investment sector of the global market finally wakes up and starts diversifying their asset base to commodities and precious metals.

Real Central Bank Buying

It has been widely suggested by several research analysts that officially reported central bank gold purchases materially understate the true scale of buying in this particular historical cycle.

In other words, the chart above may only show part of the story.

Goldman Sachs recently published research suggesting that China’s actual gold accumulation is significantly larger than official data implies, with their estimates pointing to purchases potentially 10 times greater than formally reported.

By tracking flows through the London OTC market, analysts believe China has been quietly accumulating substantial volumes of gold, as part of a deliberate strategy to diversify reserves, reduce reliance on the U.S. dollar, and strengthen its sovereign balance sheet with an asset carrying no counterparty risk.

That is the key point.

Central banks are not buying gold because they suddenly discovered a shiny metal.

They are buying gold because they understand the fragility of the paper monetary system better than anyone.

Central Banks Remain Committed to Gold

Global central bank interest in gold remained strong in Q1 2026, despite an increase in reported sales, particularly from Turkey and, to a lesser extent, Russia.

Even with those sales, central bank demand remained firmly positive, with net purchases of 244 tonnes in Q1, up +17% quarter-on-quarter.

So while the market obsesses over short-term price action, the real buyers, the sovereign buyers, continue doing exactly what matters:

Accumulating physical gold at every opportunity.

Disclaimer: This commentary is provided for informational purposes only and does not constitute financial advice or a solicitation to buy or sell any investment products. While every effort has been made to ensure accuracy, Indigo Precious Metals Group and Auctus Metal Portfolios accept no liability for any losses arising from reliance on the information contained herein. Clients should seek independent professional advice before making any investment decisions.