China Enters Currency War

Devalues Yuan By Most On Record In A Single Day

The 1.9% devaluation sends the Yuan to its weakest since April 2013.

Update: The Chinese currency complex is collapsing… 12 month NDFs just hit a new 5 year lows against the USD – biggest plunge since Lehman

Asian currencies are getting hit hard today since the China announcement, for example US$ against Sing$ has hit a new recent high of 1.40 from a low of below 1.32 just a few months previous. That is a 6% move in just the last 3 months. Last year US$ ag Sing$ was trading at 1.24 – that is a 11% devaluation in the last 12 months.

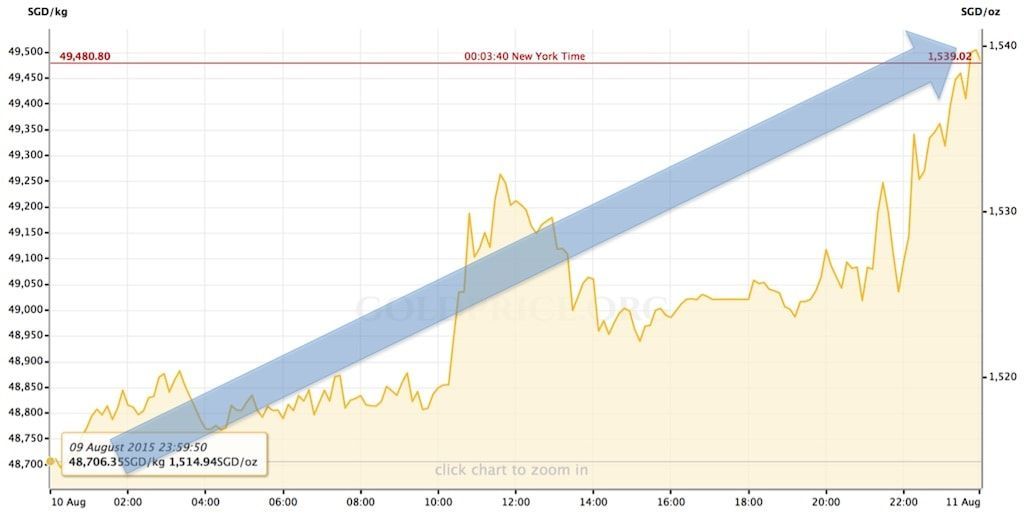

Gold against Sing$ Chart – Last 12 hours

Sing$ has dropped against the Gold price over 3 % today as I write this, presently trading at 1565 . ( Updated 6pm 11th August)

Back to China….

Chinese stocks are holding on to modest losses in the pre-open as, just as we have been warning, the PBOC weakens the Yuan fix by the most on record.

As we first warned in March, and as became abundantly clear over the weekend when weaker than expected export data as well as the steepest decline in factory gate prices in six years underscored the extent to which the engine of global growth and trade has officially stalled, Beijing has no choice but to join the global currency wars, as the yuan’s dollar peg will ultimately prove to be too painful going forward. The renminbi has appreciated on a REER basis by double digits over the past 12 months, weighing heavily on already depressed exports. With multiple policy rate cuts having proven to be largely ineffective at resurrecting the flagging economy, the PBoC, despite the notion that this represents a “one-off”move, has been left with little choice. The bottom line: the danger posed by the country’s deepening economic slump now definitively outweighs the risk of accelerating capital outflows – especially after the latter moderated slightly in Q2.

As we noted over the weekend, “one can repeat that the PBOC will have to lower rates again until one is blue in the face (even as out of control soaring pork prices make it virtually impossible for the local authorities to ease any more), the realty is that Chinese QE is now inevitable. Why? Because while the government is already clearly buying stocks thereby validating the “other” transmission mechanism, the only thing the PBOC still hasn’t tried is to devalue the yuan. As global trade continues to disintegrate, and as a desperate China finally joins the global currency war, it will have no choice but to devalued next.”

Recall also what SocGen’s Albert Edwards said some five months ago:

We have long believed that China’s growth and deflation problems will necessitate a devaluation of the renminbi in a strong dollar environment. There is mounting evidence that this process may already be underway as the currency falls to a 28-month low against the dollar…

In the current deflationary environment the Chinese authorities simply can no longer tolerate the continued appreciation of their real exchange rate caused by the dollar link.

Given The IMF’s delay decision, it seems that PBOC has decided maintaining a stable FX rate in the face of collapsing stock market is no longer in its best interest. Although the spin is already out…

- *PBOC SAYS YUAN EFFECTIVE FX RATE STRONGER THAN OTHER CURRENCIES

- *PBOC SAYS TODAY’S YUAN FIXING IS ONE-OFF ADJUSTMENT

- *CHINA TO KEEP YUAN STABLE AT REASONABLE, EQUILIBIRIUM LEVEL

- *PBOC SAYS YUAN EXCHANGE RATE DEVIATED FROM MARKET EXPECTATION

As Morgan Stanley warns however, this has much broader implications for China…

The potential for US$4.8 billion in losses for every 0.1 above the average EKI could have significant implications for corporate China in its own right, as could the need to post collateral on positions even if the EKI level is not breached.

However, the real concern for corporate China is linked to broader credit issues. On that, it’s worth reiterating that the corporate sector in China is the most leveraged in the world. Further loss due to structured products would add further stress to corporates and potentially some of those might get funding from the shadow banking sector. Investment loss would weaken their balance sheets further and increase repayment risk of their debt.

In this regard, it would potentially cause investors to become more concerned about trust products if any of these corporates get involved in borrowing through trust products. In this regard, this would raise concerns among investors, given that there is already significant risk of credit defaults to happen in 2014.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery in Singapore, Malaysia or safe storage at Free port Singapore.