British & the Likely Labour Government

Posted by Martin Armstrong 20th April 2015

QUESTION: Mr, Armstrong; you wrote that Labour has a slight advantage. I assume you are including the SNP of Scotland since they use to be Labour. They were not included in the Telegraph poll. Is this the reasoning behind your warning that the British pound is likely to fall to par?

ANSWER: Yes. The SNP appears poised to take 56 out of 59 seats. This is a hard turn to the left for Scotland after the rigged elections. Ms Sturgeon is pledging to fight for public spending increases and end cuts across Britain. What she does not get is that Britain already has the highest debt out of all of Europe on a per capita basis.

I do not see where there is any practical hope for Britain. This election is too early. In this case, they are likely to step on the accelerator and go over the cliff at top speed.

The pound is already turning negative on our Energy Models and it has elected the four minor Monthly Bearish Reversals. A monthly closing below 14790 for April should warn of a low in June.

From the beginning of this year I warned the markets would churn into May. Everyone knows something is wrong. They just cannot put their finger on it. But yes, a Labour victory is possible with a solid backing from the SNP. That should give a wake-up-call to capital for you can expect their secret agenda is to adopt the US system of worldwide taxation. They too are proceeding with the same line of thinking – when broke, raise taxes.

A clarification on UK’s Continued Borrowing Binge. by Indigo Precious Metals

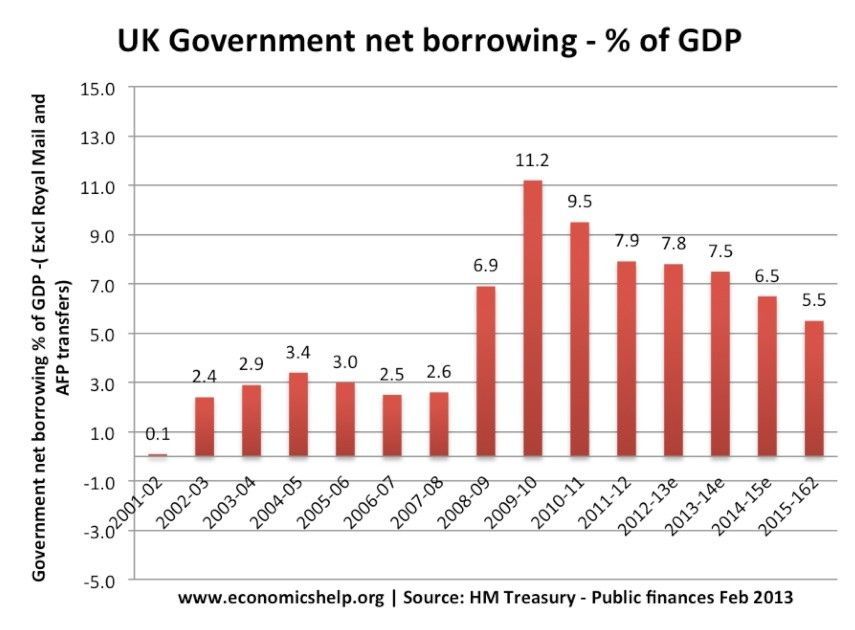

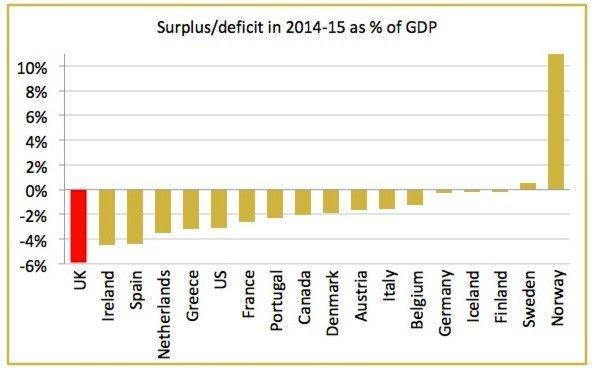

UK budget deficit is reported at 6.8% of GDP in 2014 and a great deal higher than most economies including those in the Eurozone (even Greece or Spain) and will not have much chance at balancing the deficit until at least 2019. However with the political parties battling each other while making spending promises to the electorate, any balancing seems extremely unlikely. The public sector debt is now near 100% of GDP – and this still does not portray the real debt picture in the UK (not the net debt figure of 78% that the government likes to quote).

The UK’s economic growth pick-up is based not on increased business investment or exports, both are in the doldrums. It is founded on a government-stimulated housing boom through cheap credit and subsidies for home purchasers, against all the principles of a ‘free market’. This has driven home prices through the roof, predominately in London.

This expansion is unproductive and fictitious and cannot sustain real growth. UK productivity growth is near non-existent, well in fact to be more accurate productivity is presently recorded lower today than in 2007, Total factor productivity – which includes not just the contribution of workers but also of capital and management – fell by 0.1pc in 2014, by 0.4pc in 2013 and by 1.5pc in 2012. This was the first time since 1992 that the UK has suffered three consecutive annual falls on this measure, and this is when the UK is supposedly 5 years out of the crisis and have achieved economic escape velocity ?

The UK government’s forecast of a huge expansion in exports is also somewhat of a pipe dream – to say the least.