The Top 10 Reasons For Investing in Platinum

Incredible Value Trade

By David Mitchell 26th July 2022

CLICK HERE to download the full colourful pdf report, otherwise continue to read below….

Summary Coverage

1) Platinum is Extremely Oversold.

2) Growing Supply-Demand Deficits in Platinum

3) A Shortage of Physical Supply (Backwardation)

4) Higher Loadings of Platinum in Catalytic Convertors & Substitution of Platinum for Palladium, EV limitations on global fleet of vehicles

5) Platinum Demand from The Hydrogen Economy Is Growing Rapidly

6) Rapid Advances in Hydrogen Fuel Cell Vehicles That Utilize Platinum

7) Considerable Ore Grade Degradation for Platinum at Mine Production Level

8) 90% of the World’s Platinum Supply Comes from Just 3 ‘Politically Precarious’ Countries: S. Africa, Zimbabwe & Russia

9) The Energy Crisis with Eskom in South Africa (Rolling Blackouts and Ever Higher Load-Sheddings) Pose Substantial Risk to Annual Mining Output

10) The Platinum-Gold Ratio is Heavily Oversold

There exists an incredible investment value trade in Platinum today that many investors have yet to fully comprehend the extent of how exciting this trade is setting up to be.

Client feedback currently centres around the belief that the continued growth in Electric Vehicles (EVs) will negatively impact the demand for Platinum. However, the opposite is true when it comes to the ongoing industrial demand for Platinum.

In 2016, we rigorously examined a similar macro-industrial picture in Palladium and especially in Rhodium; and advised our clients to enter into these trades at that time. Both investment trades proved to be hugely profitable with Palladium rising +450% and Rhodium rising +1,700% into 2021.

NB: Our clients are now out of these trades as we are forecasting Palladium will move into a supply-demand surplus, and whilst we expect Rhodium to remain in deficit, the major price revaluations have already taken place.

Editor Disclaimer: It is important to stress that we are not proposing that clients will see the same level of returns seen from Palladium and Rhodium between 2016 and 2021. However we can demonstrate that a very similar macro-industrial supply-demand picture is now building in Platinum.

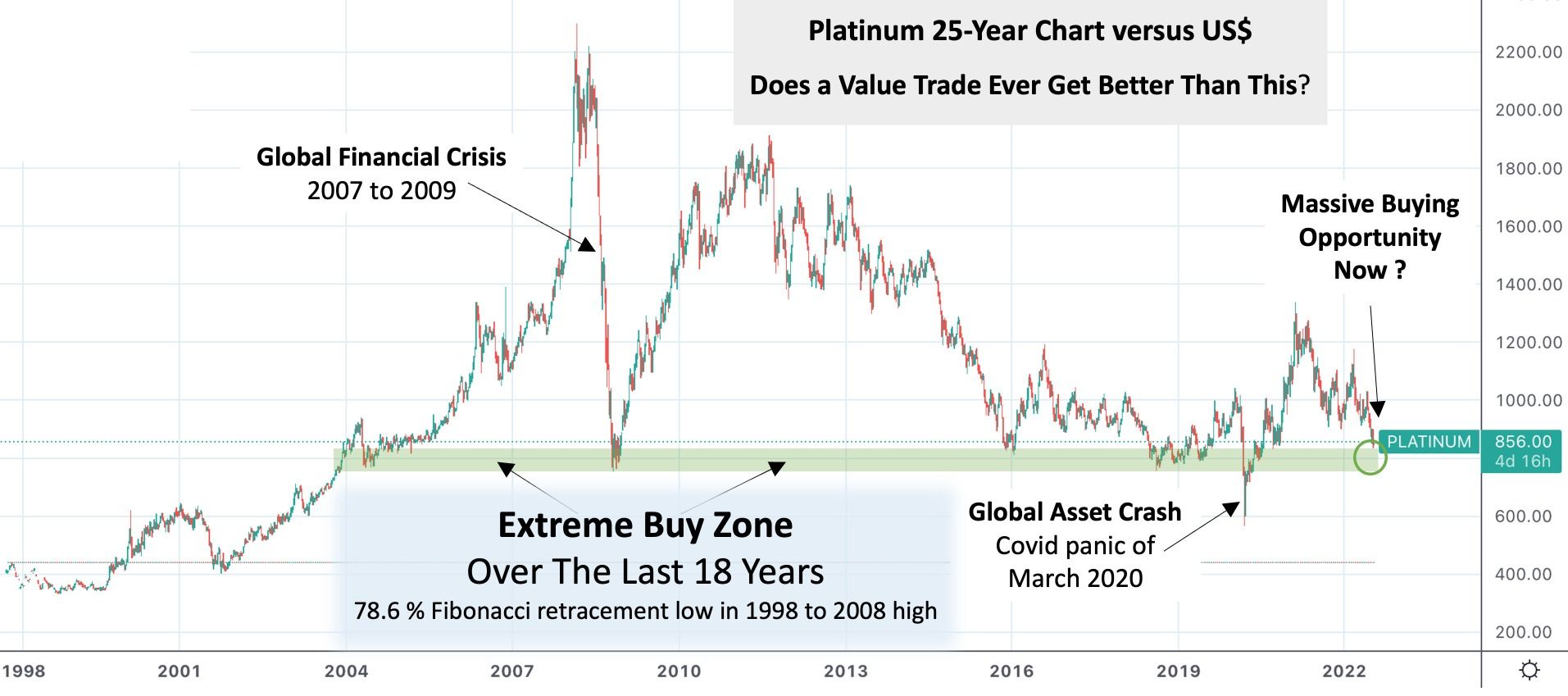

What has inspired me to put together this short article, is the foundation of the long-term price chart for Platinum and the fact that the obvious buy-zone over the last 18 years has produced significant returns for clients. The situation today however, is even more extreme…

The Extreme Buy Zone highlighted in the chart above has proved time and time again as a fantastic opportunity for investors and we have once again (this July) hit this all-important resistance level. The only time in the past 18 years that we have broken this level for Platinum, was during the global asset market “covid panic crash” of March 2020, which was then rapidly reversed within just 7 calendar days.

Top 10 Reasons to Buy Platinum Therefore Are:

1) Platinum is Extremely Oversold.

From a technical standpoint, Platinum is extremely oversold at these price levels as can be seen from the chart above. Whilst this does not necessarily mean that Platinum cannot remain highly oversold for a longer period of time, the 18-year chart clearly demonstrates that buying Platinum in the low to mid US$800s per Troy Ounce (Toz) has indeed proven to be a very rewarding investment strategy.

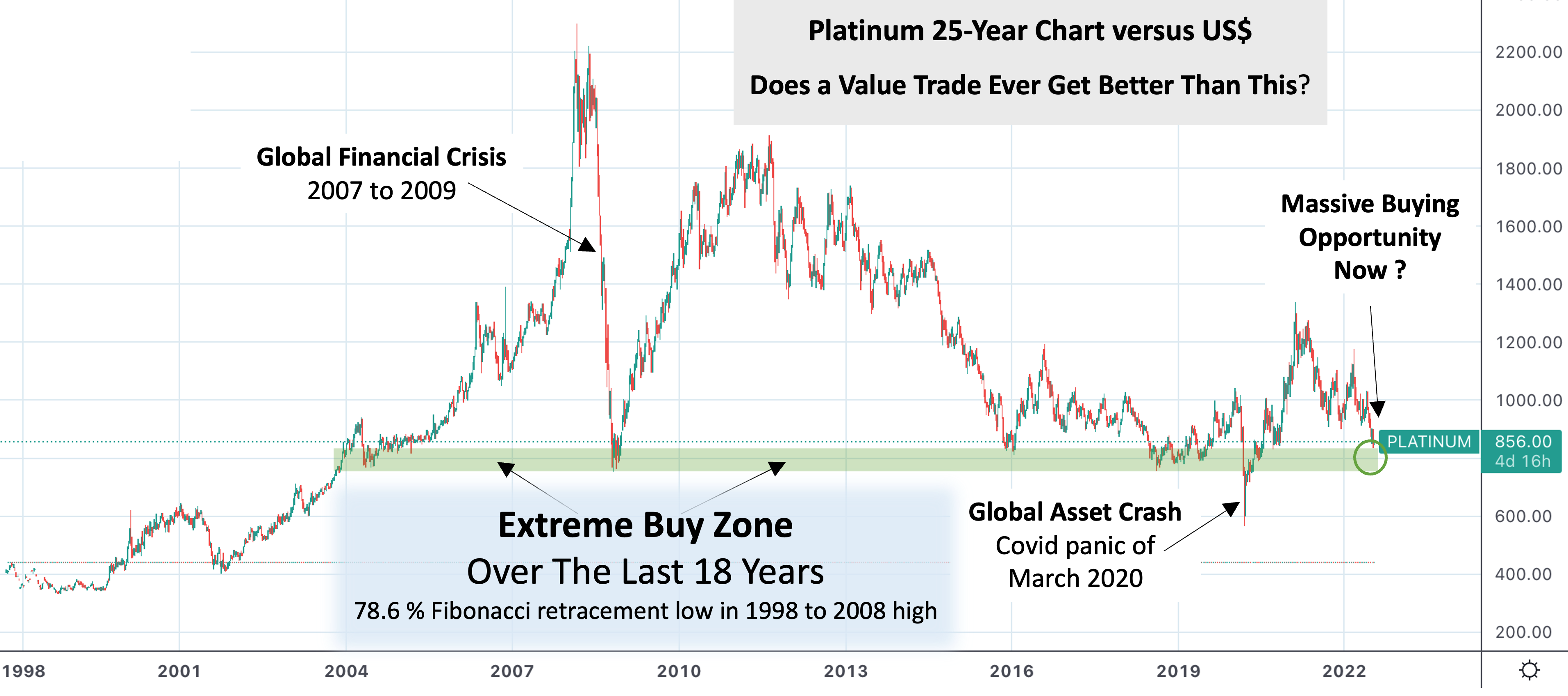

Whilst considering the price chart above, it is also very important to note that the value of currency itself has depreciated dramatically since 2004; as can be clearly seen with the ‘M3’ Broad Money supply of the OECD, which expanded by nearly 4X during this precise 18-Year period.

Note: The Organization for Economic Co-operation and Development (OECD) is a unique forum including the governments of 37 democracies with market-based economies including the USA. This of course further enhances the value of Platinum in FIAT currency terms.

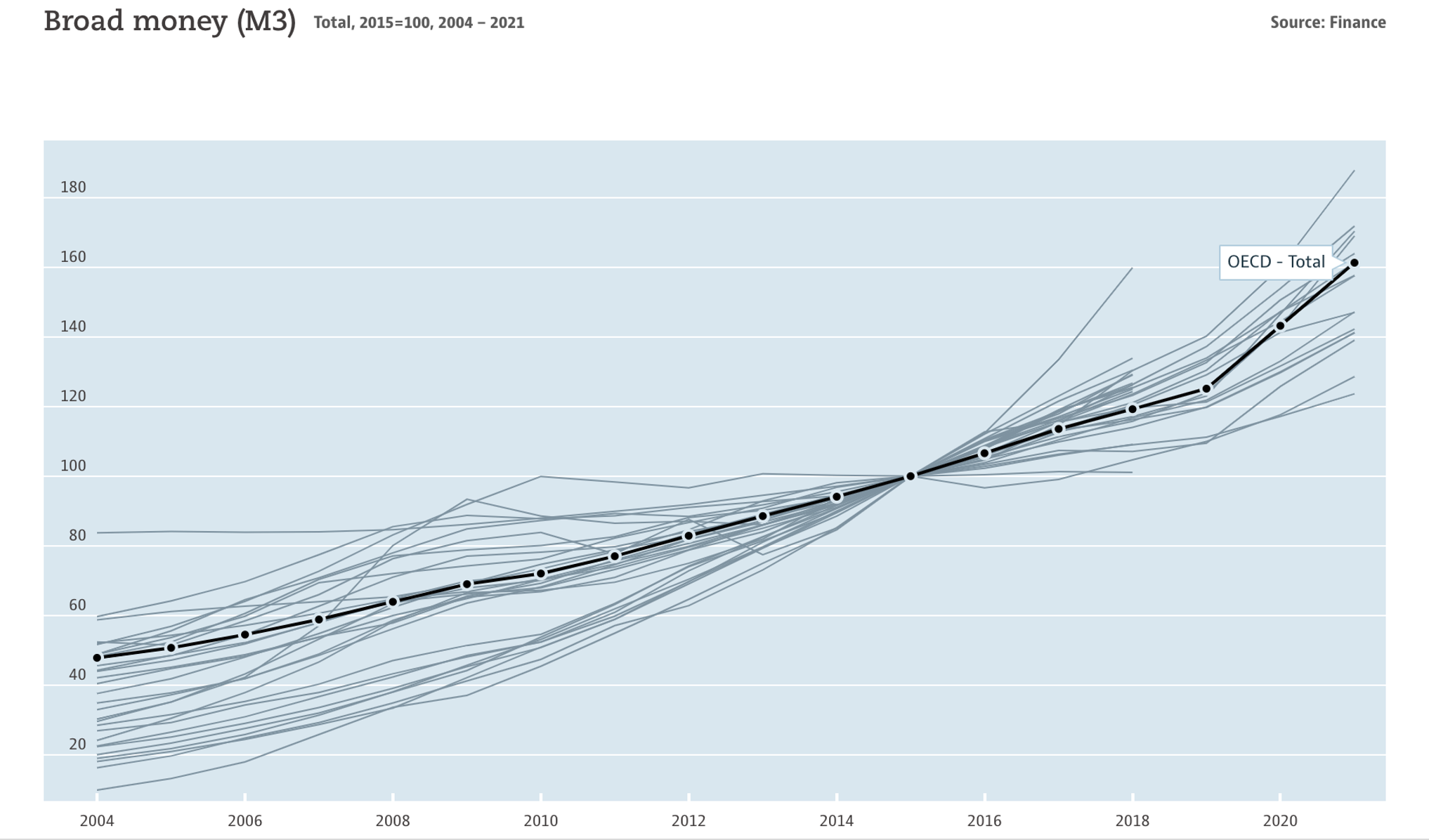

2) Growing Supply-Demand Deficits in Platinum

A modest global supply-demand deficit in Platinum was reported by the World Platinum Investment Council in 2021 (when including China’s imports in 2021 of circa. 1.3 million Toz to 1.4 million Toz).

Headlines from many of the world’s foremost research agencies have similarly confirmed this clear deficit analysis, as identified by the World Platinum Investment Council’s latest report “Platinum Q1 Quarterly Analysis and Forecast for Supply & Demand in 2022”.

The hard data points to modest Platinum deficits in 2023 and 2024 with increasing and materially deeper deficits into 2025 and 2026. It is noteworthy that our supply-demand data does not include China’s platinum imports in excess of identified demand, which deepened the 2020 deficit and also moved the overall Platinum market from a major surplus in 2021 into a modest deficit.

Deficits (or rather additional demand over and above available supply) is being filled by draining all existing and accessible stockpiles that are above ground, which are becoming increasingly limited in both size and availability at a price the market wishes to sell at.

As can be seen from the chart below using data from the US Department of Energy, the blue line exhibits significant and growing deficits moving forwards as platinum demand soars above the supply (blue line)

Source: US DOE, 22nd February 2022. Graphics transcribed by Dr David Davis using estimates.

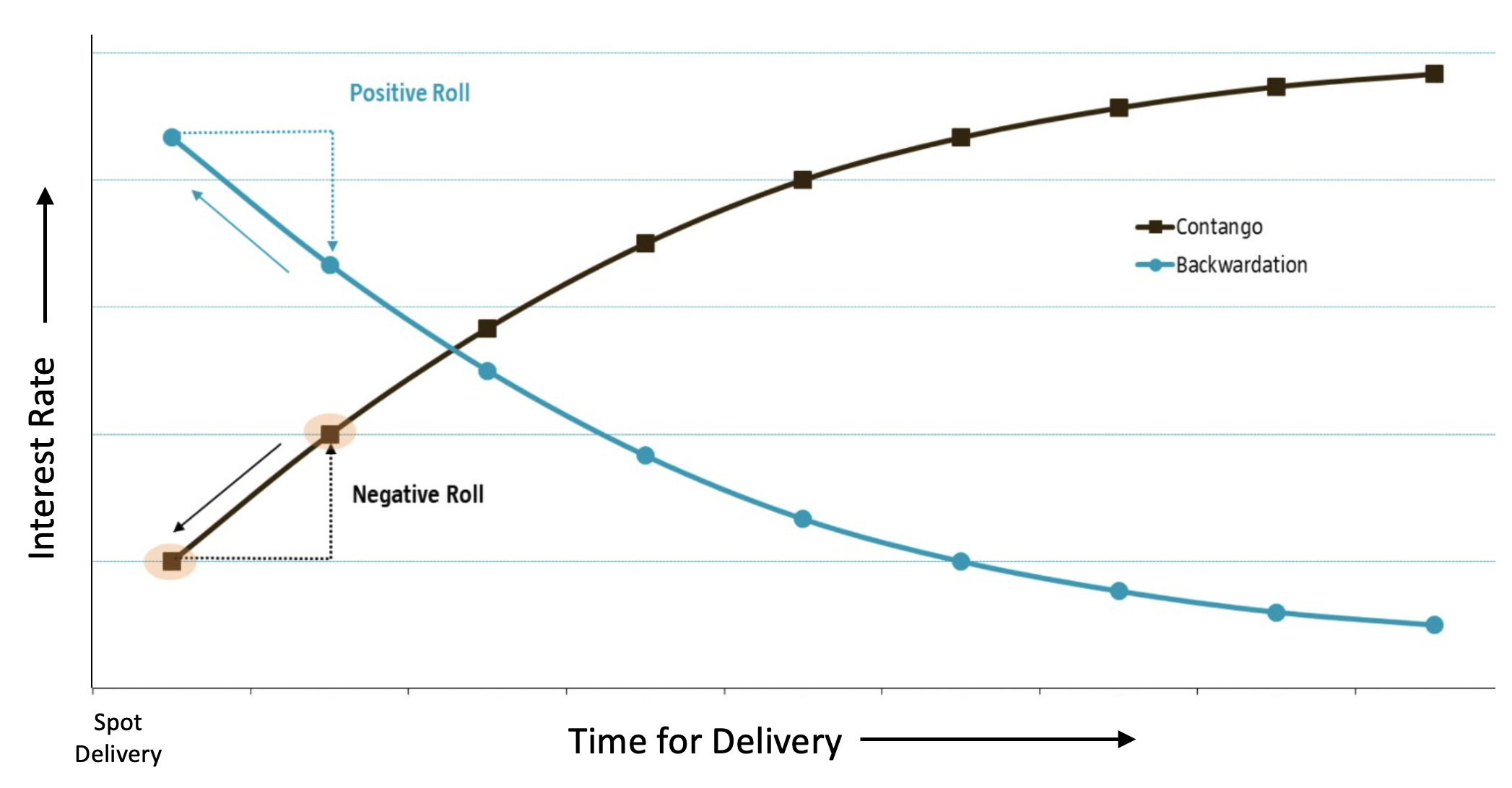

3) A Shortage of Physical Supply (Backwardation)

Backwardation in the Platinum market is still significant and this clearly demonstrates a tightness or shortage of physical metal supply. Put simply, backwardation describes a situation whereby the short-dated or cash price of a commodity is trading at much higher interest rates than the forward price of delivery in say 3 months or longer (for example). See demonstration chart below.

4) Higher Loadings of Platinum in Catalytic Convertors & Substitution of Platinum for Palladium

Catalytic Platinum Demand. The catalytic mix is changing rapidly with Platinum substituting Palladium on a near one-to-one basis due to economic price drivers (with Palladium being over 2X the price of Platinum). Hence, demand for Platinum is increasing dramatically alongside the recovery and growth in automotive demand; as well as higher Platinum loadings being required to meet ever-tightening global emissions standards (including increased CO2 efficiencies).

The WPIC have noted in one of their recent reports, that higher substitutions and loadings of Platinum within the catalytic convertor will more than offset any ongoing risks to vehicle production and the corresponding automotive demand for Platinum.

Definitions: Plug-in hybrid electric vehicles (PHEV’s and MHEV’s) are a combination of gasoline and electric vehicles, so they have a battery, an electric motor, a gasoline tank as well as an internal combustion engine and catalytic (that demands usage of Platinum).

It is very possible that we could see a swing back towards diesel, given that diesel engines are circa. 20% lower in CO2 emissions as compared with equivalent gasoline engines. This argument is support by the fact that NOX emissions for new diesel vehicles have already been addressed by the design of modern catalytic converters.

EV Facts: The trend of electrifying the automotive industry will continue, however this is being heavily tempered by the fact that not all vehicle roles, geographies or national grids are indeed suitable for vehicle battery electrification. Widescale and independent research agencies are united in their outlook that internal combustion engine vehicles will continue to remain a core part of the global drivetrain for the next 20 years at least.

In 2021 total electric vehicles sold were just 7.9% of the total volume of vehicles sold globally. This volume includes passenger vehicles, light trucks as well as light commercial vehicles. EV sales include fully electric car and plug-in hybrid-gasoline combustion engine passenger cars. Hybrids also demand high loadings of Platinum.

5) Platinum Demand from The Hydrogen Economy Is Growing Rapidly

The global hydrogen economy has been significantly underestimated and the demand curves for Platinum in this new arena are demonstrating significant growth. Demand for Platinum from the hydrogen economy is expected to dramatically rise into 2030, further pressuring the already tight physical market.

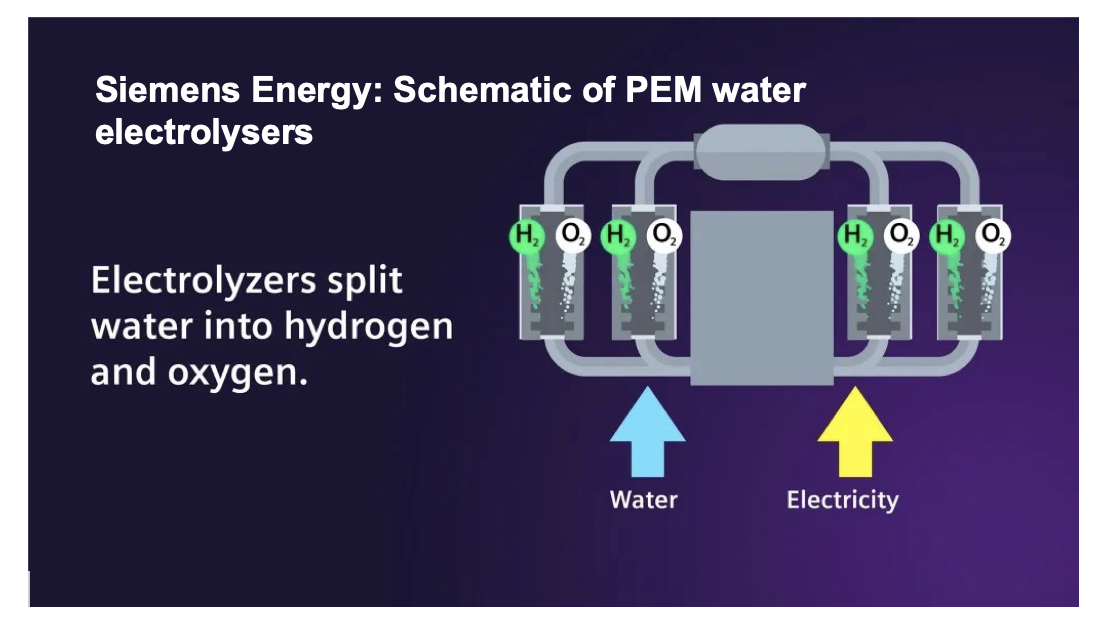

Global decarbonisation has become synonymous with Platinum and green hydrogen. But what is green hydrogen? Green hydrogen is defined as hydrogen that is produced by splitting water into both hydrogen and oxygen using renewable electricity (electrolyser). Green hydrogen has significantly lower carbon emissions than grey hydrogen.

Just as Platinum demand has been inextricably linked to the introduction of lower vehicle emission standards (which have been progressively tightened through worldwide regulation since 1970), so green hydrogen has now become a key pillar of decarbonisation for the whole industry, and Platinum is a critical raw material required for this process.

The WPIC expects Platinum demand from electrolysers to rapidly grow over the next 15 years, along with substantial technology development over this period. This will include the volume of Platinum that could potentially be used in alkaline electrolysers. According to the WIPC, electrolysers use relatively small amounts of Platinum and are built to last, meaning infrequent replacement. Nevertheless, the quantum of Platinum used to produce green hydrogen increases significantly over time when alternative and additional industrial uses are taken into account.

6) Rapid Advances in Hydrogen Fuel Cell Vehicles That Utilize Platinum

Hydrogen Fuel Cell technologies are advancing quickly, utilising the technology advances that have been made in EV’s with electric motors. But rather than relying on a bank of batteries for the energy source, it relies on stored hydrogen, which again requires platinum for the electrolysis process in the fuel cell that converts hydrogen into electrical energy, with only heat and water as the sole emissions by-product.

Hydrogen fuel cell cars have been on the market for a number of years now and both Japanese and Korean conglomerate car manufacturers are making rapid advances. Watch this Explanatory Video:

7) Considerable Ore Grade Degradation for Platinum at Mine Production Level

Ore grade degradation in Platinum at mine production level will have a significant negative effect on global production levels over the next 10 years. The decline in global Platinum mine supply has not been given the attention it deserves by many industry research organisations and investors. After all, the market balance equation and resultant impact on the price of Platinum relies on both supply and demand metrics. These organisations appear to ‘shy away’ from this aspect; preferring to focus almost entirely on the demand side of the supply-demand equation.

We know that a deficit in the overall market balance will put significant upward pressure on the price of Platinum. Global platinum mine supply depends heavily on the South African Platinum Group Metals (PGM) mining industry and to a lesser extent on the Russian (PGM) mining industry, which respectively supply some 73% vs. 10% of global Platinum mine supply.

Platinum (& Platinum Group Metal) reserves are undergoing a long-term structural change with much depending on ore reserve replacement, which requires enormous capital expenditure. The long-term decline in Platinum mine supply is a result of a combination of factors, which include the declining grade of the three key reefs over time, the unequal depletion of reserves as well as the historical evolution of the mining mix ratio of the PGM reefs to higher mining ratios of the UG2 Reef (which has much lower Platinum grades when compared to the Merensky Reef). This is despite the enormous 6E resources reported by the platinum (PGM) mining companies in their annual mineral reserve and resources reports.

It is important to note that there are additional factors which are likely to accelerate the decline in Platinum supply, in particular, the loss of PGM supply associated with South Africa’s looming energy crisis (Eskom – the national power utility board). Furthermore, the political climate remains non-conducive to the commitment of large amounts of capital, resulting in a distinct lack of appetite from investors.

Platinum and Palladium exports from Russia to the West remain at risk due to UK/EU/US sanctions, which are likely to continue to experience supply chain issues. Challenges in logistics, deliveries of equipment, spares and consumables due to the sanctions imposed on Russia, will take their toll on supply from the medium to long term. Similarly, plans to develop the Chernogorskoye deposit and Southern part of Norilsk-1 will also depend on the company’s ability to overcome these sanction related limitations. In this regard, the continuity of risk to primary supply from Russia is very much to the downside.

8) 90% of the World’s Platinum Supply Comes from Just 3 ‘Politically Precarious’ Countries: S. Africa, Zimbabwe & Russia

With 90% of the world’s Platinum supply coming from just 3 countries: S. Africa (72%), Zimbabwe (7%) and Russia (11%), this geographical and political concentration of supply can be described as ‘precarious’ at best.

9) The Energy Crisis with Eskom in South Africa (Rolling Blackouts and Ever Higher Load-Sheddings) Pose Substantial Risk to Annual Mining Output

The infrastructure across South Africa is under severe risk of collapse, almost entirely led front and centre by the failures of the national utility provider of S. Africa – Eskom. This impending calamity appears to be quickly unravelling. An initial inexorable and slow decline of output coupled with regular and escalating national blackouts are having an immediate domino effect on S. African mine production.

As Ernest Hemingway once wrote in one of his novels, “How did you go bankrupt?”; “Two ways,” he replied “Gradually, then suddenly.”

We have written and published many articles on Eskom, but the widespread crisis within South Africa involves rail networks, road infrastructure, civil unrest, labour strikes and deep-seated issues across all utility companies. Former CEO of The Post Office in South Africa Mark Barnes, Says South Africa is Dangerously Close to Collapse. Watch Here.

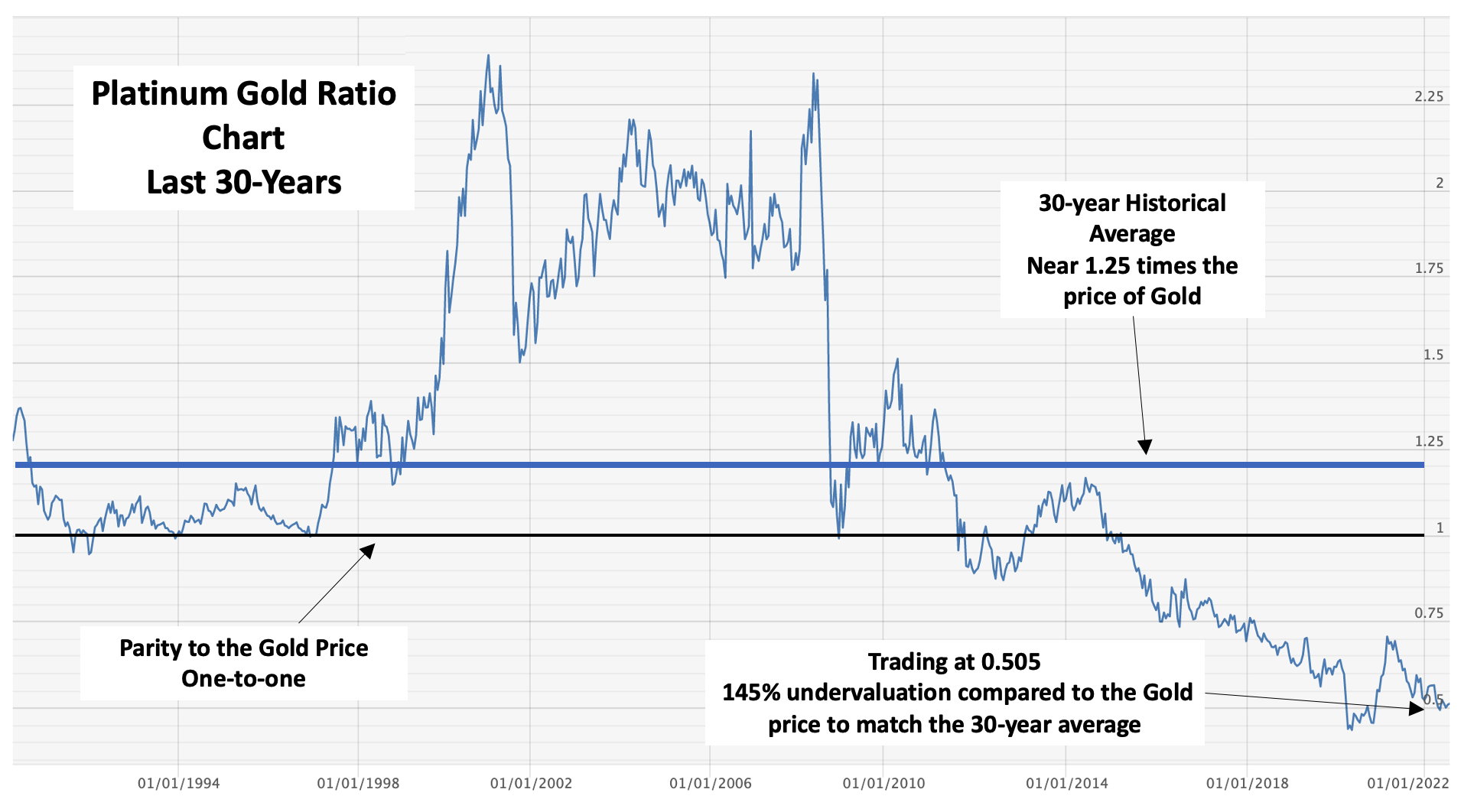

10) The Platinum-Gold Ratio is Heavily Oversold

The Platinum-Gold Ratio is heavily oversold trading at just 50% of the price of gold. With Platinum being 15 times rarer than Gold, it has enjoyed a price premium over Gold for nearly all of its history, spanning the last 120 years.

A simple re-calibration of the price ratio based on its rarity and cost of production would signal a tremendous upswing in the price of Platinum; also given the expectation that we have for the price of Gold to continue higher over the next few years.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery across the world.

Consider the safest option of segregated, allocated vault storage at Le Freeport Singapore with Indigo Precious Metals.

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.