The Big Picture: the “quiet” tape is not calm, it’s coiling

The fundamental picture is shifting rapidly across the commodity complex , and particularly across precious metals. Ironically, the longer price action stays moribund in a range (as it has for the last ~7+ weeks), the greater the risk that the next move is not incremental… but violent . Range-bound markets don’t stay polite forever, they compress, then they release.

Yes, classical technicians across the market are presently arguing for one more “wave” lower in precious metals, before new highs. I’m not dismissing that . But the growing imbalance beneath the surface makes the downside argument increasingly fragile. The setup is becoming too obvious in my book: the longer the lid is held down, the bigger the spring-load becomes.

The War Shock: shipping disruption is not a headline, it’s a structural reset

The war and the disruption to key shipping routes, including the effective closure of the Strait of Hormuz are already creating serious medium-to-longer-term consequences across:

• Energy and refined fuels

• Global agriculture and fertilisers

• Helium and critical industrial gases

• Logistics and freight costs

• Industrial production and input inflation

• Capital flows and currency stress

In my view, the scale of these knock-on effects is being materially underestimated by both the investment community and mainstream media.

This is not a short-term disturbance. This is the kind of structural shock that forces new valuation models, new supply chains , and new pricing regimes.

Strait of Hormuz: the numbers that matter

Iran has implemented what is, in real-world terms, an effective closure of the Strait of Hormuz since 28 February 2026 . As of 27 April 2026 , that places us around the 60th day of disruption and closure, with no clear end point in sight.

What does that mean in practical terms? The Strait is not “just another headline”, it is a critical artery . The estimates that matter are large:

• ~20% of global oil and energy flows

• ~25% of global LNG flows

• Significant global flows of Helium

• Roughly 35%–40% of global fertiliser supply (including nitrogen fertilisers such as urea and ammonia)

You don’t need a PhD in geopolitics to see what happens next: higher energy costs cascade into everything , food, transport, industrial margins, and ultimately inflation expectations.

The Energy Transition: demand isn’t slowing, it’s accelerating

At the same time, the world continues to move toward higher electricity demand and heavier energy usage:

• Data infrastructure expansion

• Electrification

• Re-acceleration in power build-out (nuclear, coal, gas), particularly across Asia and China

That trend drives intense focus on next-generation energy storage , and solid-state batteries sit right in the centre of that conversation.

Solid-State Batteries: why silver’s role becomes “strategic”, not optional

Solid-state batteries replace liquid electrolytes with solid materials and are widely viewed as a major next-gen technology due to potential advantages:

• Higher energy density

• Faster charging

• Improved safety

• Longer life cycle

Samsung’s research has highlighted all-solid-state designs using a silver-carbon composite layer to improve performance and address key technical challenges.

That is where silver becomes increasingly interesting.

To be clear: silver-based SSB designs are not yet guaranteed at mass scale, but the direction of travel is what matters. If these technologies scale, silver shifts further into the category of ‘critical’ strategic industrial metal.

And it’s not as if silver is waiting around doing nothing today: industrial demand is already historically strong, and the use-case breadth keeps expanding.

The Deficit Backdrop: silver is already tight, demand is getting faster

In a world where silver has been running multi-year supply-demand deficits (five years and moving into a sixth), the key point is simple:

The industrial demand curve is not just rising, it’s steepening.

You can argue about the exact grams per application, but the direction is clear: EVs, solar, electrification, advanced electronics, and energy storage all pull the same way, toward much higher structural silver consumption.

How to recognise when the market is about to run

This is the part I care about most: the next spike higher may not be a gentle one.

When a market is structurally tight, and positioning is thin, the upside move tends to arrive as a gap, not an invitation.

Key signs to watch for:

• Strategic accumulation of physical (not “paper participation”)

• Less dependence on futures flow; more emphasis on physical delivery-based exchanges

• Premiums widening where real demand shows itself first

• Inventory drawdowns becoming persistent, not episodic

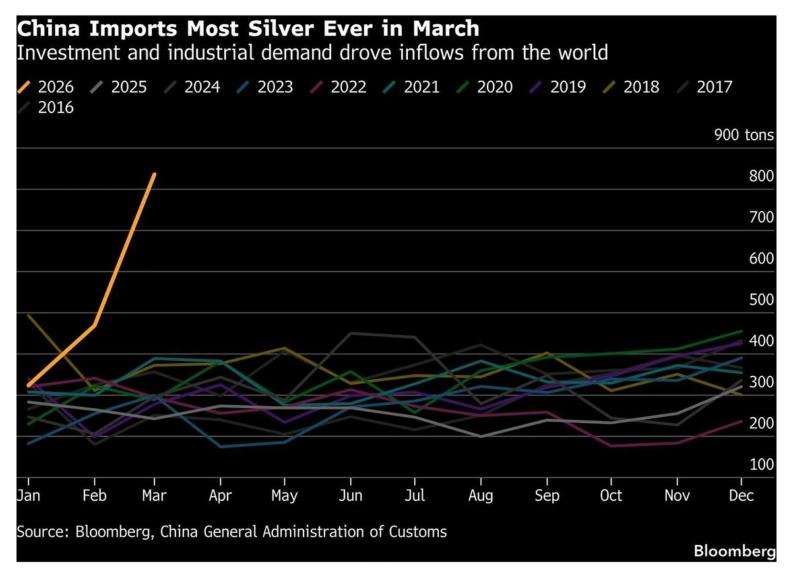

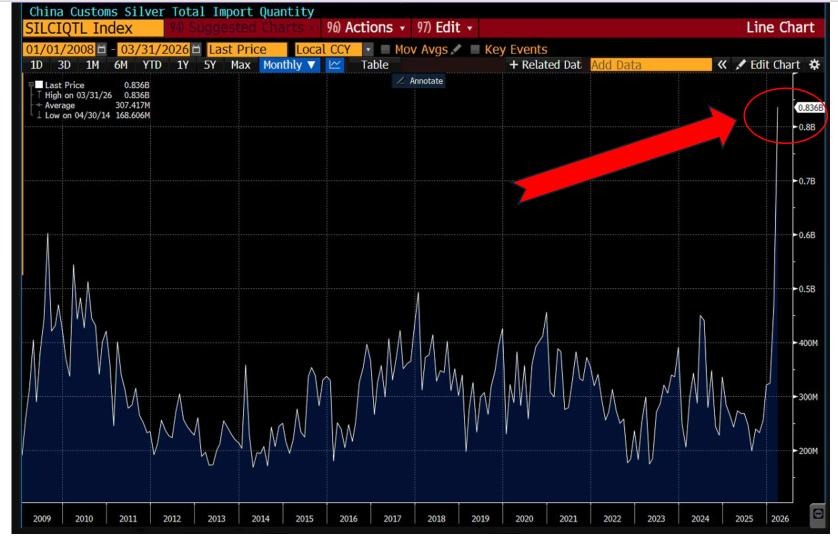

I’ve included two charts in this note, both showing the same message: China’s silver imports have surged. And at the same time, the Shanghai physical market continues to trade at a notable premium versus Western paper pricing.

That’s not noise. That is the market telling you where the real pressure is forming.

The Monetary Layer: debt is exploding, debasement is the “pressure valve”

Now add the final ingredient: global debt and deficits continue to expand, and central banks, openly or indirectly, are already being forced into measures that amount to monetary expansion support (money printing) for their debt markets.

This is the core point:

commodities don’t need a perfect world, they thrive in an unstable one.

Energy disruption + industrial demand + supply tightness + monetary debasement is not a “maybe”. It’s a real-world framework.

And frameworks like this don’t resolve with prices drifting sideways forever. They resolve with repricing.

China is already a global top-three silver producer, yielding 109.3 million ounces as of 2023, trailing only Mexico presently. China also controls an estimated 60% to 70% of global refined silver production.

And now its silver imports explode!

While the Shanghai physical silver exchange is still trading at over 13% above the paper exchanges of the West.

The end game of a violent revaluation in the commodity complex and particularly precious metals is without argument.