Forget Rate Hikes, Ray Dalio Says QE4 Is Coming;

Warns World Is At The End Of Debt Supercycle

Ray Dalio, founder of the $165bn hedge fund group Bridgewater Associates and the head of the world’s largest hedge fund just relased a note in the last week to his clients.

He delivers one of his usual sermons about the economy as a perpetual motion machine, affected by central banks, and where interest rates are supposed to boost asset returns by being below “the rates of return of longer-term assets.”

None of that is terribly exciting and it is in fitting with what Bridgewater has said for a long time (incidentally, it is curious that just over the weekend, the FT released a piece in which a “US asset manager warns over risk parity” which is what Bridgewater’s bread and butter is all about).

What is exciting is the following part:

That’s where we find ourselves now—i.e., interest rates around the world are at or near 0%, spreads are relatively narrow (because asset prices have been pushed up) and debt levels are high. As a result, the ability of central banks to ease is limited, at a time when the risks are more on the downside than the upside and most people have a dangerous long bias. Said differently, the risks of the world being at or near the end of its long-term debt cycle are significant !

That is what we are most focused on. We believe that is more important than the cyclical influences that the Fed is apparently paying more attention to.

While we don’t know if we have just passed the key turning point, we think that it should now be apparent that the risks of deflationary contractions are increasing relative to the risks of inflationary expansion because of these secular forces. These long-term debt cycle forces are clearly having big effects on China, oil producers, and emerging countries which are overly indebted in dollars and holding a huge amount of dollar assets—at the same time as the world is holding large leveraged long positions.

While, in our opinion, the Fed has over-emphasized the importance of the “cyclical” (i.e., the short-term debt/business cycle) and underweighted the importance of the “secular” (i.e., the long-term debt/supercycle), they will react to what happens. Our risk is that they could be so committed to their highly advertised tightening path that it will be difficult for them to change to a significantly easier path if that should be required.

Leading to the conclusion that “We Believe That the Next Big Fed Move Will Be to Ease (Via QE) Rather Than to Tighten“

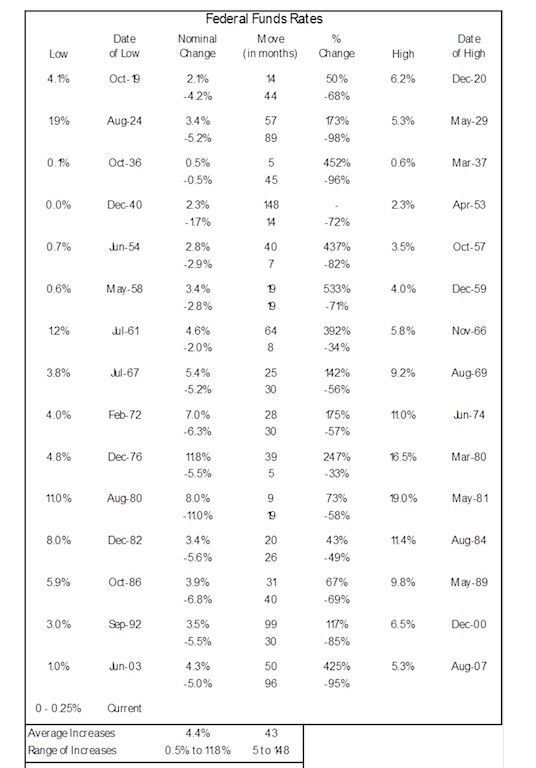

He shared a table which showed that the average tightening over the past 100 years was 4.4% and pointed out that the smallest was 0.5% in 1936, the same year that the U. S. was undergoing a deleveraging of the long term debt cycle.

He reiterated

“To be clear, while we might see a tiny tightening akin to what was experienced in 1936, we doubt that we will see anything much larger before we see a major easing via QE,” he wrote.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery in Singapore, Malaysia or safe storage at Free port Singapore.