As I wrote early last week, with silver trading around 75 US$ and general market sentiment negative with Chinese New Year holiday in full affect, what stood out to me was not just the market commentary itself, but the tone behind it.

Sentiment across large parts of the market remains distinctly bearish precious metals, particularly among fund managers and financial advisers. The negativity is and was striking.

In my view, much of this stems from a very simple reality: large sections of the fund management and advisory community have largely ignored global macro dynamics completely, specifically the wider structural implications of a global debt crisis and the generational shift now unfolding. What we are witnessing is not a short-term anomaly, but a broad asset-class rotation away from highly financialised paper markets and toward tangible, real-world assets, led squarely by precious metals, which is in effect a full cycle period leading into early next decade.

Many in the traditional investment space have either missed these moves or are under pressure from clients for having done so. The easiest response in such circumstances is to label the move in precious metals a “bubble” and declare it unsustainable.

As an example, I was recently asked to respond to a short opinion piece written by a Chief Investment Officer claiming ‘silver is simply another bursting bubble’. His argument rested entirely on overlaying the recent silver chart with the final weeks of the 2000 dot-com Nasdaq bubble peak, presenting it as definitive proof.

Quite a remarkable comparison to make, and a rather superficial one at that.

There are, of course, significant flaws in the simplistic exercise of overlaying generic historical “bubble” charts onto silver and declaring speculative excess simply because the shapes appear similar.

Serious analysis requires far more than visual comparison. We assess fundamentals, cycle duration, capital flows, positioning, macro backdrop, and structural supply dynamics, not just vague chart symmetry.

Take the Nasdaq bubble of 2000. That episode formed after nearly a decade of relentless equity inflows, extreme valuations, and widespread retail participation bordering on mania. Silver, by contrast, only broke above a major structural resistance level on 10th October 2025, a level that had capped the market for 45 years. Bull markets do not typically exhaust themselves within three months of emerging from an enormous multi-decade consolidation. Historically, that is when they begin.

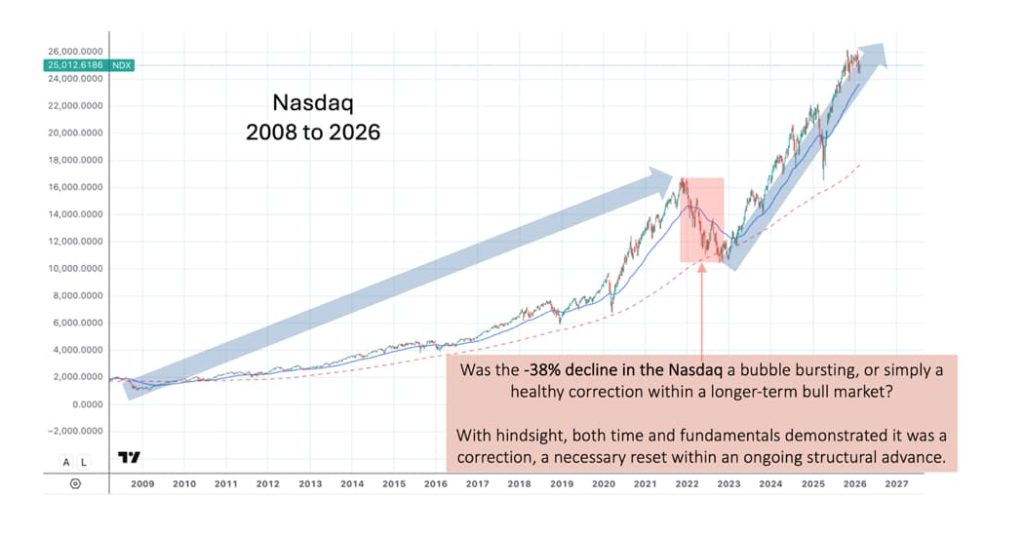

If one insists on Nasdaq comparisons, a more intellectually honest parallel might be late 2022, after 14 years of capital inflows from the 2008 low. The Nasdaq then fell roughly 38%, remarkably similar to silver’s late January 2026 correction (now labelled a “bubble bursting” from certain quarters), only for the Nasdaq to rally 2.6x from that 2022 low to fresh all-time highs.

Even so, I would argue silver’s revaluation potential into the latter stages of this cycle toward 2030 is likely to be measured in many multiples from today’s levels, as silver has not had multiple years of capital inflows

More importantly, the bubble narrative ignores several critical structural signals currently shaping the silver market:

- Persistent backwardation across portions of the forward curve

- Elevated lease rates

- Significant inventory drawdowns across major exchanges

- Extremely low COMEX participation, with open interest at the lowest levels since February 2024, weak speculative longs largely flushed out.

- A sixth consecutive year of global supply-demand deficits; the last five years of deficits collectively equal roughly one full year of global mine supply

- Declining ore grades globally

- Rapidly expanding industrial demand, which has grown from approximately 20% of total supply (including recycling) a decade ago to over 67% today

- And perhaps most critically, an increasingly fragile global financial system burdened by excessive debt and leverage, where monetary debasement remains the only viable pressure valve

These are not the hallmarks of a speculative blow-off top. They are characteristics far more consistent with the early-to-middle phase of a structural bull market.

Perhaps most telling of all is positioning. I spend a considerable amount of time presenting our research to fund managers, pension funds, family offices and private banks. The consistent conclusion is striking:

Meaningful institutional capital has not yet entered this sector in any size.

History offers a simple lesson. Bull markets rarely end in scepticism and under-allocation. They tend to conclude only after enthusiasm turns into participation, and participation turns into excess.

So it is worth asking a straightforward question:

When has a genuine bull market ever ended before institutional capital arrived?

Bull markets do not end in non-participation. They end in mass-participation and excess exuberance.

Price Volatility is Normal

When studying the 1970s bull market, a decade in which gold rose approximately 27-fold and silver 44-fold, it is important to remember that volatility was a feature, not a flaw.

During that period there were four separate corrections of 25% or more, and in 1975 the gold market retraced nearly 50%, yet the broader bull trend remained entirely intact.

Sharp pullbacks do not invalidate structural bull markets. They reset sentiment, clear leverage, and strengthen the foundation for the next advance.

The more important question is not the size of the correction, but whether the fundamental drivers of the cycle have changed, a few simple questions will answer this:

- Has the global debt burden relative to GDP disappeared?

- Will sovereign debt realistically be paid down through organic growth and productivity gains?

- Will central banks cease monetary expansion while governments continue to run structural deficits?

- Have persistent global supply-demand deficits across the commodity complex, particularly in silver and platinum been resolved?

Until the answer to those questions is unequivocally “yes,” the structural case for precious metals and the commodity complex remains intact.

Volatility is temporary.