Please note: Disclaimer at the end of this article.

It’s the Debt, Stupid ! (A play on Clinton’s phrase)

BIS complete Policy Reversal

Effect on Precious Metals

Part 2. Conclusions

Originally published in August 2013 by D Mitchell, Updated March 2015

Part 1 of this article can be found here.

My Conclusions and my comments concerning Silver / Gold.

The World’s markets have never been so asphyxiated with easy money as a whole in recorded modern history with ‘real’ interest rates in negative territory across the world.

This financial repression has decimated savers and forced Corporations, Hedge funds, Pension funds and investors into ever more risky asset classes as they continually search out yield wherever it may be. Junk Bonds and very risky investment classes have never dealt or had the availability of such low funding interest rates in modern history.

We have already seen the ramifications of this in the Emerging Markets rout in the last few months, never mind Europe.

Even the BIS have stated that just looking at USA Treasury market alone a move of 300 basis points would cause a 1 Trillion US$ loss, never mind what the moves in Corporate Debt and Junk Bond Debt market moves would cost on the back of a move in the US Treasuries. We are talking Trillions of US$ losses here, just in the USA alone.

On the back of that we have a situation where the World has the highest Debt leverage in modern history.

We are talking of a massive Deflationary event (which we have felt the immediate effects off in the last 3 years, through Commodity markets & Precious Metals under extreme pressure to the downside, unemployment levels rising world wide, manufacturing slowdowns and low to non-existent growth etc.) mixed with extreme unemployment and debt leverage and overvalued asset paper markets. A halt to money printing and a slow move to normalization of interest rates in the USA (aka 2015), which the BIS are talking about here, would cause an economic Depression of unparalleled size, if this debt mountain is tipped over.

It is a correct policy response, which should have taken place a few years ago (and in actual fact in 2005/6), now the hangover or cure will most probably kill the patient outright – so now a different policy response is required.

I do believe the Bond markets and hence interest rates are now at a critical juncture purely based of the sheer size of debt outstanding. We will most likely see a final mini spike in Bond prices (lower rates) as deflation becomes ever more apparent, but the 34-year Super Cycle in Bond markets is near over with (ending in 2015?) and rates will be moving ever higher after that.

As I see it the sovereign debt crisis will move across the world (like ripples in a pond) with emerging markets and Europe suffering initially (due to the giant US$ carry trade unwinding and Europe’s systemic crisis), eventually as the dominos fall we will see this sovereign debt disaster wash up on the shores of the USA and the final bastion of strength will fall.

The Governments of the World will not allow a Depression of enormous proportions to hit their respective economies – think civil unrest here. The Central Bank panics of 2008 will be a precursor of what will be met this time around, with even more aggressive action (i.e. Massive money printing). I do believe though in this environment rates will actually move higher due to the sheer size of debt out there (remember the Japanese debt chart above from the BIS, who would lend them money at 1% or 2% when their debt is exploding exponentially?)

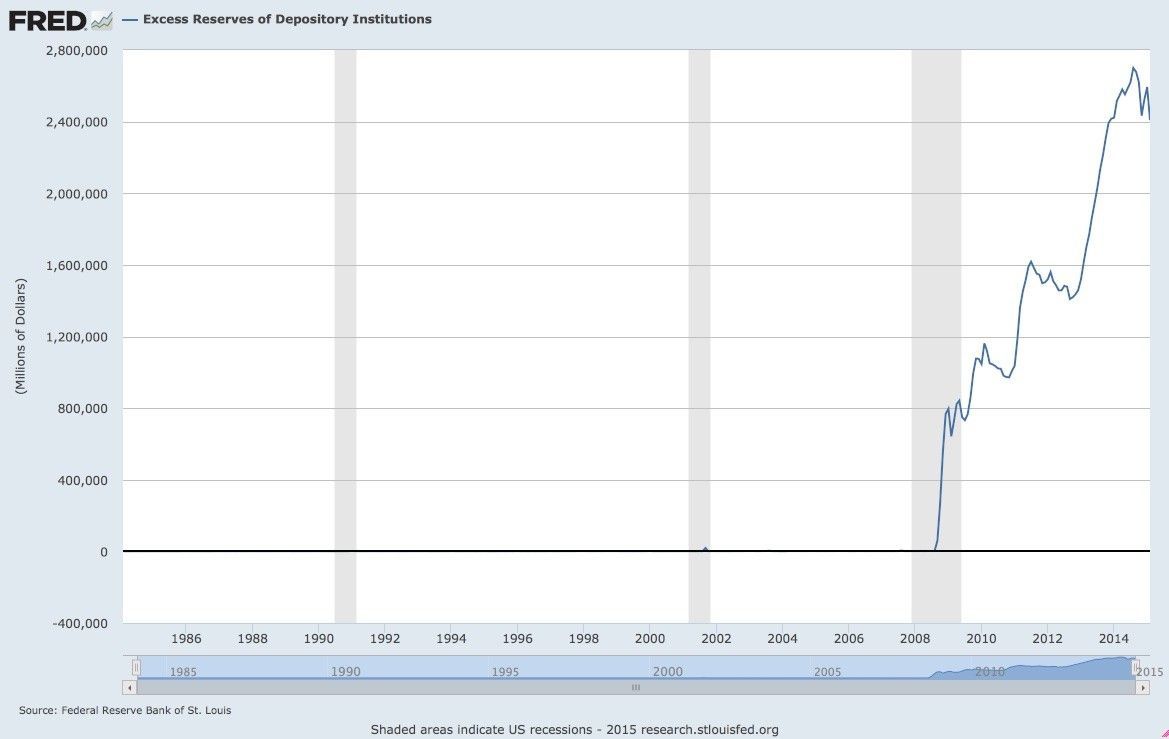

Which brings me to this chart…

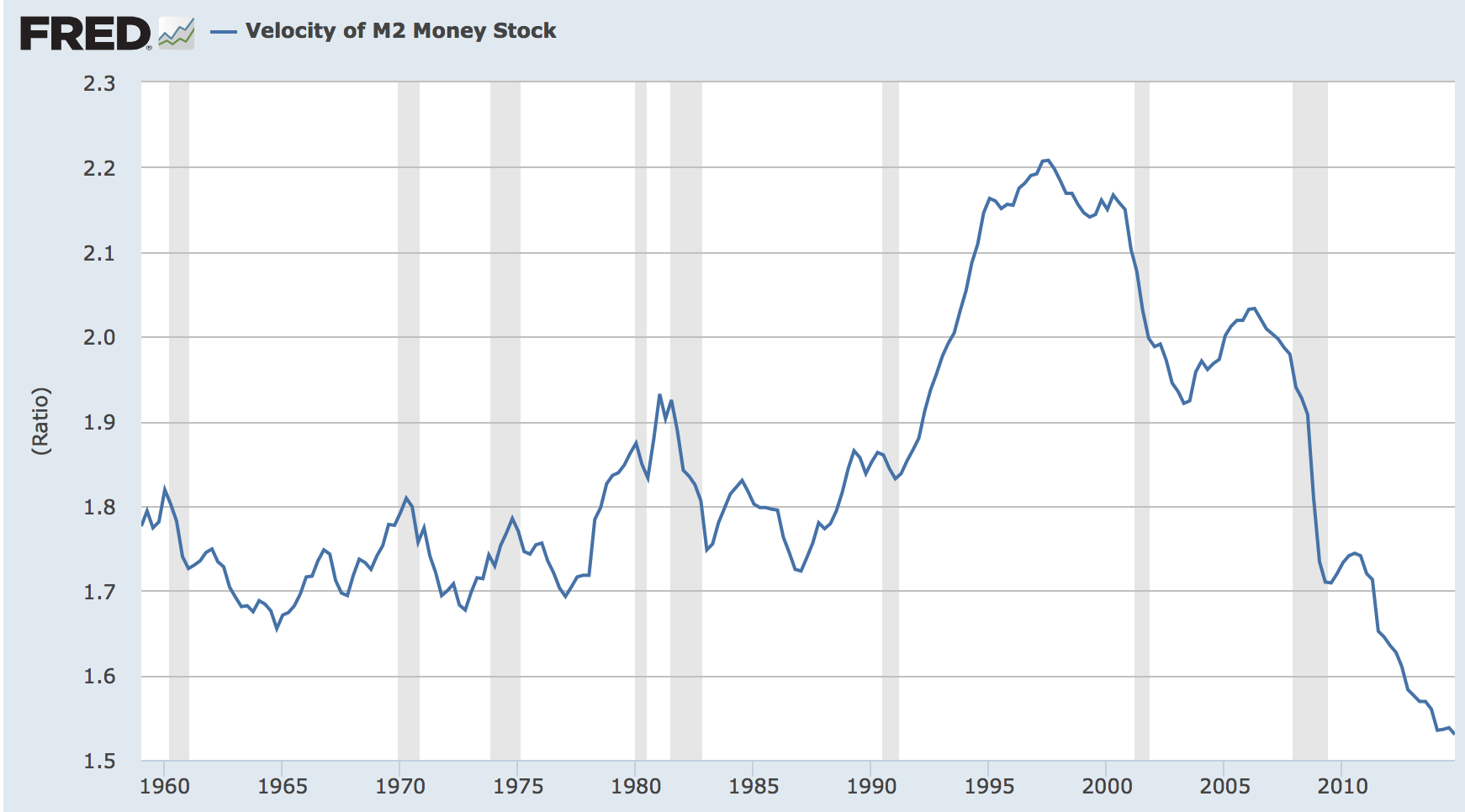

The chart above paints a picture that is really beyond what I can put in words. This is an inflationary time bomb waiting to go off at some point, especially considering the chart below. The excess Reserves that the banks hold at the FED and not presently being utilized and recorded at 2.4 Trillion US$ as of February 2015.

As money starts to move and we see policy response from the governments the Velocity of Money will reverse from all time record lows.

Precious Metals (Silver & Gold)

Remember precious metals (Gold & Silver etc.) are a crisis trade, an insurance policy used as wealth preservation vehicle with no 3rd party liability in times of systemic crisis. Would you say we are facing a systemic crisis here ?

When counterparty risks become prevalent (bonds, currency, paper assets) precious metals leap to their historical role within the monetary system.

Great Depression of 1930’s – The holding of physical gold was made illegal in the USA, but was then promptly revalued by near 70% from $20.67 to $35 by the government. This pushed investors into the prime gold miners of the day Homestake Mining and Dome Mines (for example) that appreciated near 550% (in just a few short years) between them in actual terms, in real terms that appreciation was that much greater as consumer prices and assets plummeted.

Economic crisis of the 1970’s – Gold rallied over 2,000% between 1971 to 1980.

Silver rallied over 3,000% – although selling near the highs was almost impossible.

Previous decade 2000 to 2011 – was a litany of crisis from the stock bubbles of 2000, to the twin towers, real negative interest rates and finally the 2008/09 collapse (to name but a few) – Gold rallied over 700% between 2000 and 2011.

Silver rallied 1,050 %

Now as I pointed out in part 1 we are facing a world economic disaster that is simply unprecedented in over 200 years worth of modern history due to our debt bubble ! How do you think precious metals will perform ?

China’s physical gold demand for the last several years alone has matched 100% ot total world production !

Silver

Which brings me onto Silver (Gold briefly discussed lower down in this article). This sell off that has lasted 4 years has obviously been amazingly predictive of the enormous Depression type event that is unraveling and which we are presently in the throes off.

This was not something I predicted, I simply examine the supply / demand numbers and the effects of insane policy decisions or lack thereof.

The sell off’s have actually pushed Silver 50% below full break-even production costs of prime Silver miners around the World as an average (full production costs are reported at an average cost of 24US$ in recent in-depth research of the top 12 Primary Silver Miners). Although I am sure costs are lower due to the recent oil price falls we are presently experiencing, however we are still in loss making territory for the producers (as a world average).

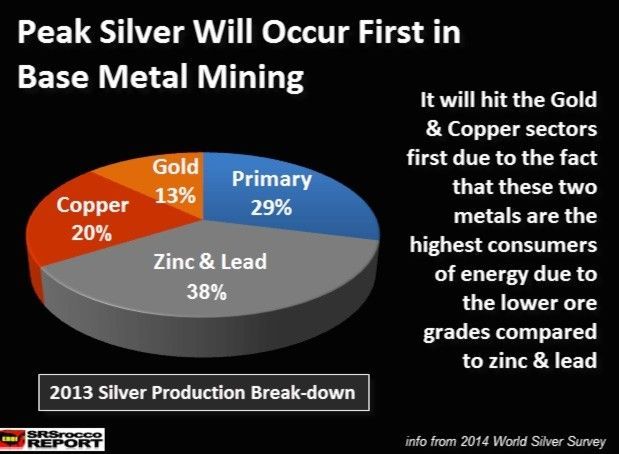

Primary Miners Real Costs by SRSrocco

Not only that but base mining groups are winding down production levels due to the economic slowdown and commodity rout around the World but especially in China – Silver is predominately produced as a by product of base metals as you can see in the pie chart below (again by our good friend SRSrocco, please see his blog).

Silver production is about to slow down dramatically over the next few years; mines cannot stay in operation producing metal at massive losses.

Remember: There are no world stockpiles of silver, the world works on ‘just in time supply’ unlike in gold. We have been suffering an actual supply/demand deficit, a shortfall of 96 million ounces in 2013 marked a significant swing from a 51 million-ounce surplus during the prior 12-month period, in turn creating the largest market deficit for five years.

Silver industrial demand is not reversing and is qualified in the industry as a wonder metal, what with it being the most reflective element on the planet, the best conductor, used in batteries for its cathode or negative side, but its most exciting industrial demand comes from its biocide qualities that no other metal on the periodical table can lay claim.

The USGS re-asserts its claim that Silver will be extinct in industrial quantities within 6 to 7 years (2020), due to its price structure (massively undervalued) and complete lack of re-cycling of industrial usage (due to it being completely uneconomical due to price) and the fact that ore-degradation is reaching complete exhaustion stage.

Silver is finite resource trading at levels that is massively below production costs and is reported by the World recognized authority United States Geologist Society (USGS) of becoming industrially extinct (due to the reasons I stated above). While miners are presently being pushed out of business and hence destruction of supply!

Gold

Central Banks around the World are accumulating Gold as part of their reserves, this overall net buying which has been taking place since 2010 has not been seen in such size since the 1960’s. Most recently, the year 2014 was the 2nd largest buying spree by CB’s in over 50 years !

The vast majority of the World’s Central Banks holds the metal as reserve requirement diversification on their balance sheets in physical holdings and have been accumulating 1,000’s of tons of the metal over just the last few years alone!

Gold / precious metals hold no 3rd party liability (unlike any other monetary asset) and considered the only true safe collateral in times of crisis.

Rather than Gold being the pre-eminent monetary inflation proof trade, it’s quite simply crisis insurance and a wealth preservation vehicle.

Along with this we are about to experience a massive destruction in the value of paper assets (going forward) along with a huge Stagflationary event (High Inflation with no growth) to help de-leverage the World from the largest debt bubble in history, which will also entail massive defaults.

Physical holdings of precious metals should be held as a diversification of your asset portfolio, especially at this moment in modern history, which in my opinion is a priority !

***

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.