Seven years of Financial Repression

Followed by Financial Martial Law

Why QE and Extreme Low Rates Do Not Work

By D Mitchell, Indigo Precious Metals, 16th August 2016

There are two sides to this coin, which we need to examine to fully realise that this zero rate policy stance has serious and unavoidable consequences…

The weight of global debt is nothing short of monstrous, having increased from a level of roughly 142 Trillion US$ equivalent at the end of 2007 to an estimated grotesque debt mountain of over 200 Trillion US$ and actually reported as high as 230 Trillion US$ (not including un-funded liabilities), easily surpassing 300% of global GDP by mid 2016. Put simply the debt expansion has far outpaced world net growth output, forcing the world’s monetary authorities into Financial Repression.

Let us first deal with the definition of Financial Repression, which is simply an expression that applies mainly to interest rates. Specifically, it’s what happens when governments, through their state central banks, keep interest rates artificially low to manage debt expansion. The policy is good for governments but it’s disastrous for savers, investors and pensioners. A policy of ultra-low interest rates via financial repression allows the sovereign debt mountain to be affordable and continually expandable !

In the 2008/09 financial crises and then the European 2011-12 debt panics, the money markets acted as they should do in a free market, specifically as a warning of a credit crunch, as trust between lenders and borrowers completely broke down. This time, though, the signs of stress throughout the system are a result of the campaign by governments direct financing of themselves, especially through QE money printing, limiting access by the private sector to funding.

Which brings us smartly into financial martial law (as some would phrase it) the next leap forward from financial repression and a much more destructive policy stance from our esteemed monetary central bankers. This next stage introduces negative interest rates to the equation. Leaping from lending money (deposit your savings) with an unstable and insolvent banking system earning extremely low rates of return (enormous risk) to having that same unstable bank actually charge you to lend money to them!

Consider that over US$13 Trillion equivalent of government sovereign debt (as of August 2016) is earning their investors (lenders) negative yields. Now the banks are directly warning their customers negative rates are coming very soon to all depositors (see UK banks), and in fact German banks are there already, see here new deposit rates to savers of -0.4%.

There are 2 further developments of financial martial law that you have to be made aware of..

Financial martial law makes it extremely difficult to get your money out of the bank in a crisis; in fact your money is locked down until the institution or banking sector in question decides how much capitalisation is required. This precedent was set in Cyprus in 2013, as depositors were “bailed-in” to help recapitalise the banking sector. To make this clear their savings were confiscated.

Bail-Ins are now law across Europe, UK, USA, Canada (Canada being implemented) and many other regions of the world.

In Europe this new law came into effect on the 1st January 2016 and is called the “Bank Recovery and Resolution Directive (BRRD)” . You are now considered a “creditor” of the bank under law.

No longer will there be a government-taxpayer funded Bail-Out, but rather Bail-In’s. The big banks will be allowed to confiscate your deposits at their discretion with no prior notice. Your compensation for the bank’s pilfering of your money is a new issuance of stock (equity) in said banks, which obviously you will be banned from selling for a lengthy period of time.

Considering the banking sectors of Italy, Spain, Portugal, Germany, France, UK (but to name just a few) are recognised by independent analysis as under extreme stress (to say the least) or simply overleveraged and severely undercapitalised should be loud alarm bells to bank depositors (savers) !

The final third stage of financial martial law is the war on cash itself ! War on cash is about forcing everyone into digital currency that can be taxed, tracked and monitored at every stage, controlled, and inflated away in order to get you to spend it faster, while paying you sub-inflation extreme low rates of interest and ultimately stopping bank-runs in its tracks.

Why QE and Extreme Low Rates Does Not Work

We have experienced enormous money printing exercises by the world central banks since early 2009 led initially by the USA Fed, in-fact at this present moment (August 2016) The European Central Bank, Bank of Japan and the BOE are buying over a US$ 180 billion of assets equivalent a month, a larger global total than at any point since 2009 – not including what China is up to, even when the Federal Reserve’s QE programme was in full flow.

- – Has world growth been re-invigorated by 5,000 year low interest rates of zero to negative ?

- – Has world growth been stimulated onto a new sustainable path by money printing ?

Of course not and this continued monetary experiment has been proven defective at best.

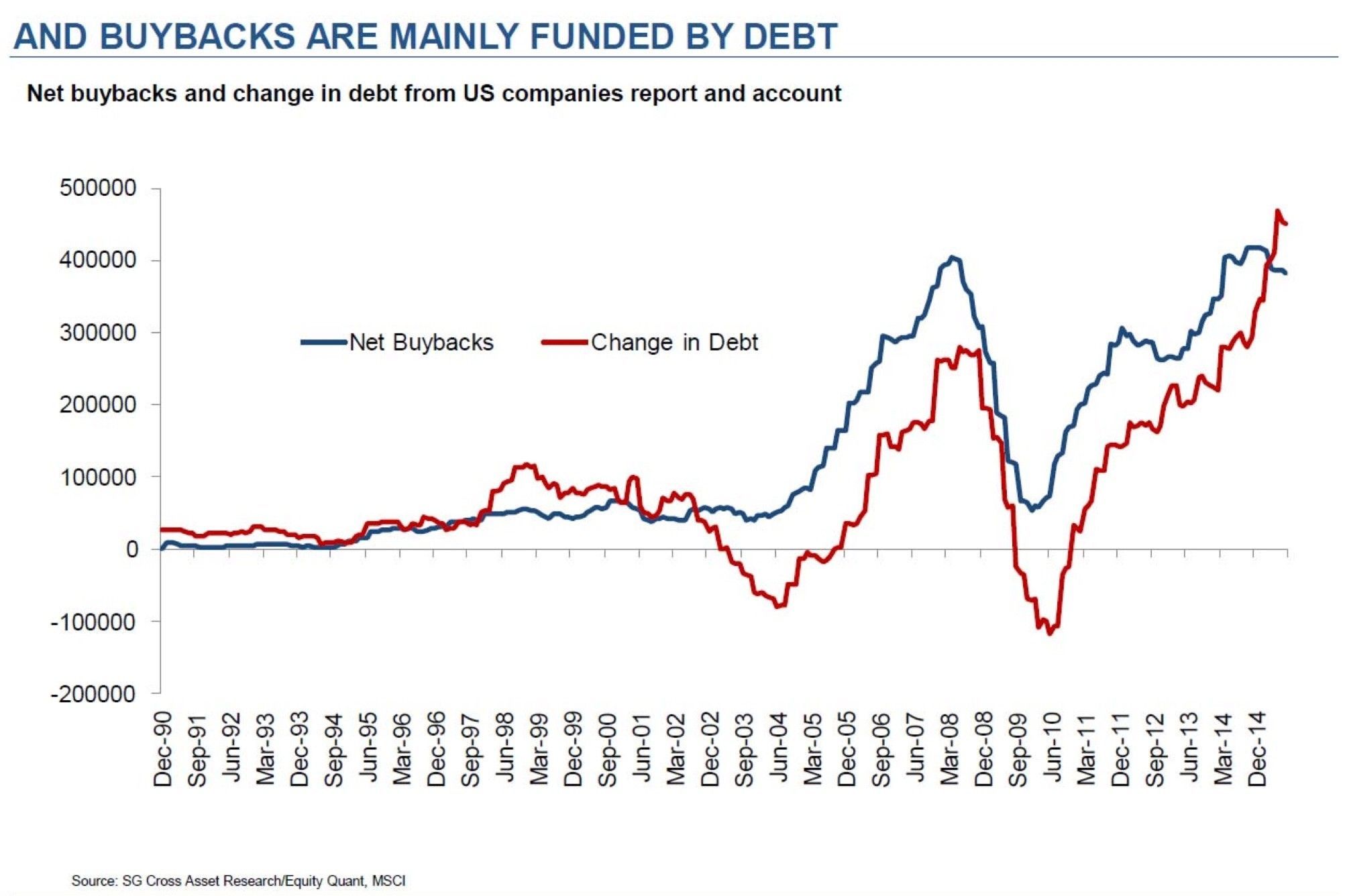

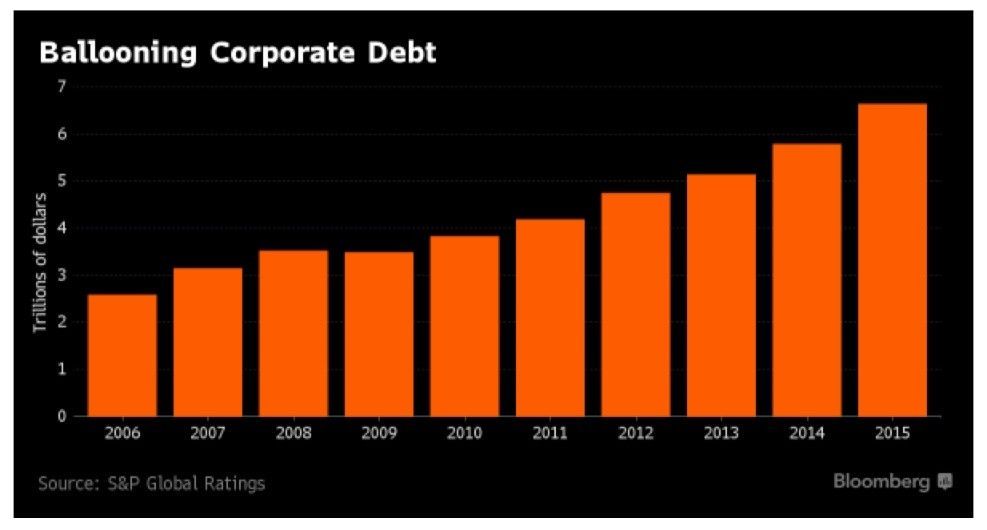

What we have experienced with zero rates and money printing is over valued property markets in certain parts of the world become ever more leveraged and overpriced culminating in extreme asset bubbles giving the false image of wealth creation ( London, Singapore, Sydney, NY, San Fran etc.. all in various stages of peaking & / or bursting ). Stock markets have also been pushed to ever-greater extremes helped by and large by corporate buybacks on the back of huge increase in corporate debt.

Unable to grow, inflate, default or restructure their way out of debt, policymakers are trying to reduce borrowings by stealth in the face of ever-expanding deficits. Official interest rates are below the true inflation rate to allow over-indebted borrowers to maintain unsustainably high levels of debt. In Europe and Japan, disinflation requires implementation of negative interest rate policy, entailing an explicit reduction in the nominal face value of debt.

Debt monetisation and artificially suppressed or negative interest rates are a de facto tax on holders of money and sovereign debt. It redistributes wealth over time from savers to borrowers and to the issuer of the currency (sovereign state), feeding social and political discontent as we are most assuredly and unquestionably seeing now.

The global economy may now be trapped in a QE-forever cycle according to policy maker’s mind-set. A weak economy forces policymakers to further implement expansionary fiscal measures and QE, around and around we go.

To give you an idea of the muted global growth and now economic slowdown over the last 7 years…

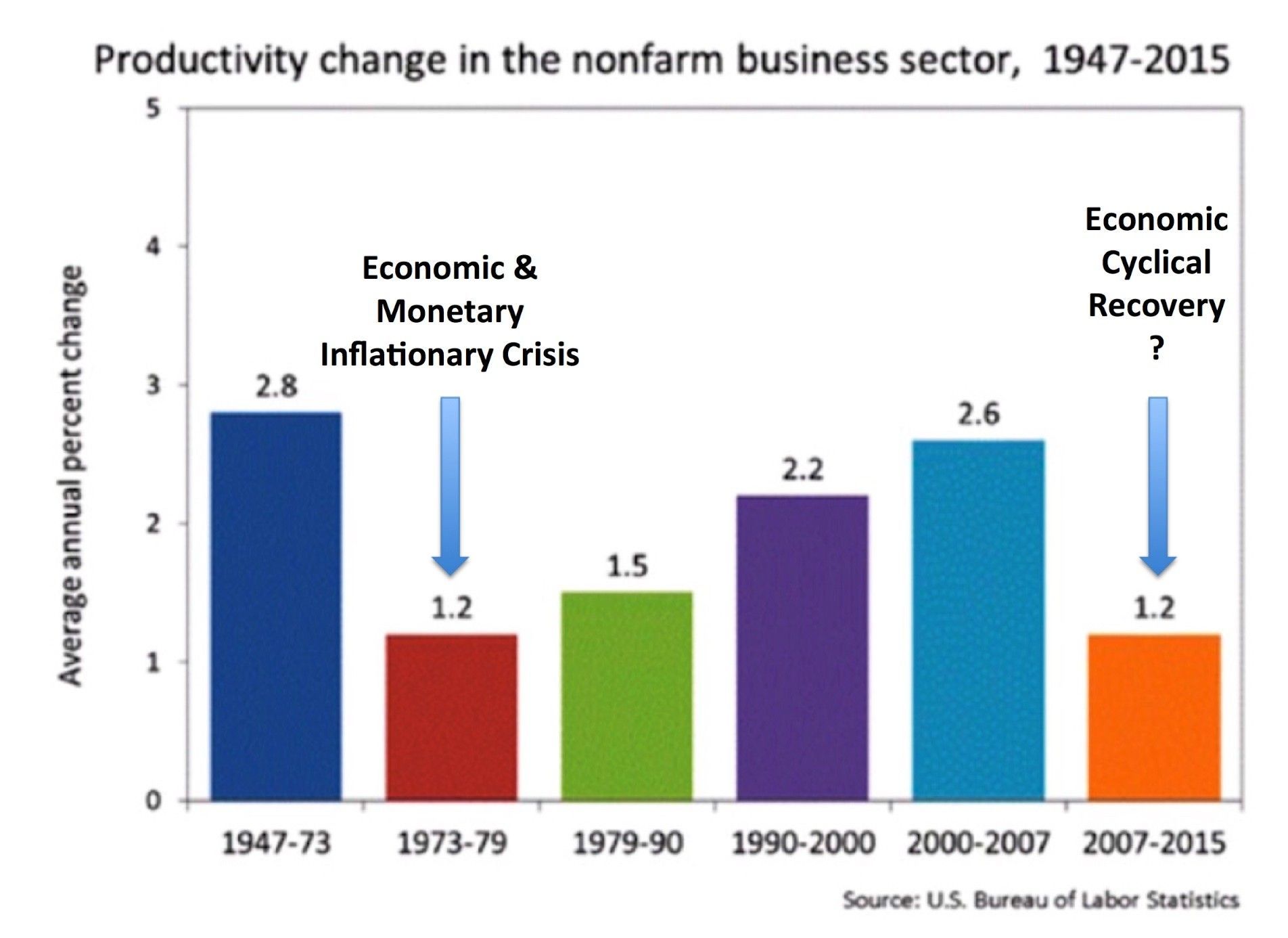

Productivity grew at an annual rate of less than 1% in each of the last five years in the USA. The average annual rate of productivity growth from 2007 to 2015 was 1.2%, well below the long-term rate of 2.1% from 1947 to 2015 and the lowest since 1973-79 at the height of that particular crisis – and we were supposed to be in the economic growth stage cycle the last 7 years!

Productivity, GDP growth, job participation (employment) rates , food stamps, Baltic Dry Index (shipping freight rates) are the lowest in 30 years, corporate profits, retail sales, factory orders (the list goes on and on) all point to significant world slowdown. What has grown substantially is world debt.

Zero rates and money printing hollows out the middles classes slowly at first but picking up speed, and it absolutely decimates pensioners. The banks themselves suffer massive damage to their balance sheets as Non-Performing-Loans alone increase due to increased debt and leverage. Pension funds and savers are pushed into ever-increasing risk across the asset spectrum in their desperate search for yields. World Pension Funds are in full crisis with ever increasing gaping holes in their unfunded pension liabilities directly caused by plummeting yields, see here.

Financial System Collapse is Unavoidable

We are now turning down in the economic cycle and global recession is again knocking on the door. Ignoring the business cycle after a near 8 year (muted) recovery and now the inevitable downturn is a serious folly.

But how does the central bankers of the world and governments respond when we enter a recession at the height of a debt bubble, zero to negative interest rates already in place and presently the world’s highest ever recorded money printing experiment ?

Debt service payments transfer income to investors with a lower marginal propensity to consume. Low interest rates are required to prevent defaults, lowering income of savers, forcing additional savings to meet future needs and affecting the solvency of pension funds and insurance companies.

Policy normalisation is difficult because higher interest rates would create a disaster for over-extended borrowers and inflict truly massive losses on bond holders. Debt also decreases flexibility and resilience, making economies much more vulnerable to shocks.

We see this effect today, with the gap between rich and poor widening dramatically. It is simply monetary policy that impoverishes the masses, more surely than death or taxes.

Once this market turns lower within a greater sovereign debt crisis (the greatest bubble every recorded) where is the ammunition to fight the downturn exactly ?

Central banks assume they can achieve their 2% inflation targets with impeccable precision, which is beyond the realms of reality. Decades worth of deficit spending, surging debt to GDP ratios and a gargantuan increase in central banks’ balance sheets and leverage will eventually lead to a significant erosion in the confidence of central bankers themselves to maintain the purchasing power of our fiat money. Therefore, inflation won’t just miraculously stop at 2%; it will eclipse that level and continue to rise.

The other side of that coin is the fact sovereign bond yields are now so low and at such preposterous extremes that when inflation truly picks up the mass exodus of the long side of the bond markets is going to be truly spectacular (think a dam bursting), taking interest rate yields up many 100’s of basis points very quickly indeed as investors capitulate on their bond investments.

As yields rise debt servicing payments will only confirm debt-saturated governments and industries as insolvent. This in turn forces the central banks to increase money printing to purchase more debt in the vain attempt to keep not only debt yields (interest rates) low but support collapsing debt markets and currency value, further eroding any confidence in the monetary system itself, around and around we go !

The Bond market has morphed into a weapon of mass destruction, complacency by investors at this time is hazardous to the extreme.

The tide is going out rapidly, especially for central banks that have run out of room for further can kicking. Interest rates can’t go much lower and QE just adds to the debt mountain, inflates asset bubbles and worsens moral hazard in the financial system itself.

It seems our date with destiny lies with a sovereign debt collapse leading into a collapse of paper currencies (inflation leading into extreme high rates of inflation, destruction of currency value).

Considering the worlds economic conditions, the perilous consequences of financial repression and rapidily inflating debt loads, we strongly believe a diversification into physical gold and silver, held outside of the banking system within segregated allocated vault storage is essential. We advise ‘at the very least’ a 15% allocation of your portfolio into physical metals at this time. If you require any advice then please contact us at Indigo Precious Metals.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery in Singapore, Malaysia, UK, Europe or worldwide.

Consider the safest option of segregated, allocated vault storage at Freeport Singapore with Indigo Precious Metals.