Debt Bubble Update:

Puerto Rico Defaults, China Debt Load Continues To Inflate

IPM Note : We have reported on the World Debt situation many times (see here, here, and here), in fact we have been banging on about this situation for the last 5 years. Why you may ask do we keep mentioning this subject on a precious metals site ? Simply because the coming explosion in Soveriegn Debt markets world-wide will have very profound effects on all of us, be it investments or job prospects, breakdown in currency unions, civil unrest – the list just goes on.

We all have to be extremely aware of how this coming storm will affect us, what will be the repercussions and how can we side step the worst of it (none of us can avoid this completely).

First Default By U.S. Commonwealth In History: Puerto Rico Fails To Make Required Debt Payment

Via Zerohedge

Over the weekend Puerto Rico was supposed to make a modest principal and interest payment of some $58 million due on Public Finance Corp. bonds, which however few expected would be satisfied. As a reminder, on Friday, Victor Suarez, the chief of staff for Governor Alejandro Garcia Padilla, said during a press conference in San Juan that the government simply does not have the money.

Moments ago Melba Acosta, president of the Government Development Bank, confirmed as much, when he announced that only $628,000 of the $58 million payment, or just about 1%, had been paid.

Below is the full statement from Acosta on the service of PFC Bonds:

Today, Government Development Bank for Puerto Rico (“GDR”) President Melba Acosta Febo issued the following statement on the service of Public Finance Corporation (PFC) bonds:

Due to the lack of appropriated funds for this fiscal year the entirety of the PFC payment was not made today. This was a decision that reflects the serious concerns about the Commonwealth’s liquidity in combination with the balance of obligations to our creditors and the equally important obligations to the people of Puerto Rico to ensure the essential services they deserve are maintained.

“PFC did make a partial payment of Interest in respect of its outstanding bonds. The partial payment was made from funds remaining from prior legislative appropriations in respect of the outstanding promissory notes securing the PFC bonds. In accordance with the terms of these bonds, which stipulate that these obligations are payable solely from funds specifically appropriated by the Legislature, PFC applied these funds—totaling approximately $628.000—to the August 1 payment.”

As the NYT adds, this is “a startling admission from the governor of an island of 3.6 million people, which has piled on more municipal bond debt per capita than any American state.”

More:

A broad restructuring by Puerto Rico sets the stage for an unprecedented test of the United States municipal bond market, which cities and states rely on to pay for their most basic needs, like road construction and public hospitals.

That market has already been shaken by municipal bankruptcies in Detroit; Stockton, Calif.; and elsewhere, which undercut assumptions that local governments in the United States would always pay back their debt.

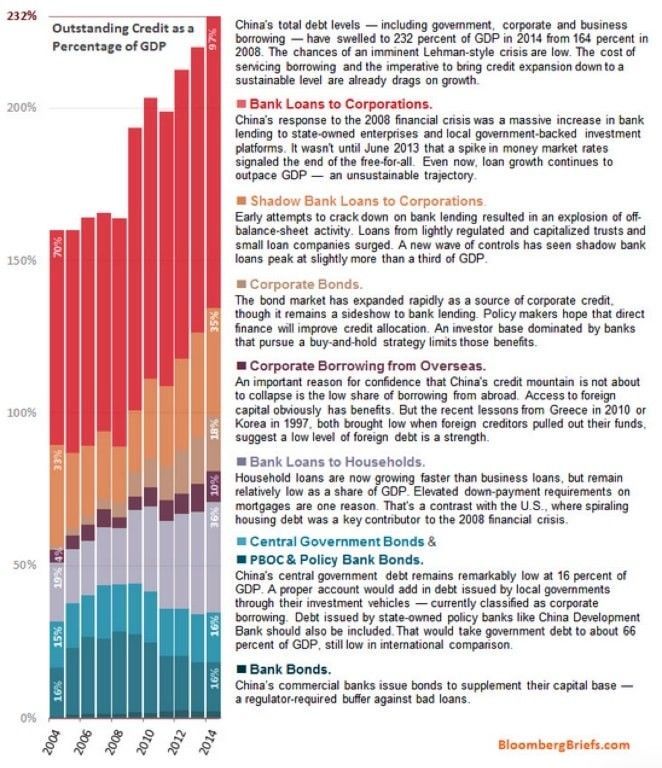

China’s US$23 Trillion Debt Pile

As Zerohedge reports on China

Back in April, we highlighted Beijing’s “massive debt problem“, noting that as of last year, total debt in China amounted to some $28 trillion when you include government debt, corporate debt, and household borrowing.

As Bloomberg noted at the time – and as we’ve discussed extensively – Beijing is facing the virtually impossible task of trying to de-leverage and releverage at the same time.

“Various parts of the government don’t always seem to be working from the same playbook,” Bloomberg observed, before quoting Credit Agricole’s Dariusz Kowalczyk who pointed out the “obvious contradiction between attempts to deleverage the economy and attempts to boost growth.”

Indeed, there are times when the scale seems to tip in favor of deleveraging. For instance, Beijing has recently shown a willingness to tolerate defaults and the case of Baoding Tianwei Group Co even suggested that in some instances, state-affiliated companies may not receive immediate government support. Nevertheless, the abrupt 180 on LGVF financing and the transformation of the local government debt restructuring initiative into the Chinese version of LTROs betrays the extent to which China is still reluctant to deleverage its economy in the face of flagging growth.

Against that backdrop we bring you the following graphic from Bloomberg which breaks down China’s massive debt pile and shows the degree to which it’s grown over the past decade.