9 Trillion US$ Carry Trade That May Take The World Economy Down

What is it exactly?

Written by D Mitchell of Indigo Precious Metals 15th March 2015

Broadly speaking, the term “carry-trade” simply means borrowing at a low interest rate and investing in an asset that provides a higher rate of return.

This in turn has evolved into a global tide of money that borrows money in a very low yielding currency (that is supported by the country in question that supports a lower or soft currency to boost their own economy) and then converts that borrowed currency into a higher yielding currency to invest it for much higher returns, for example bonds, corporate debt, property, businesses etc.

You can in effect get a much higher leverage on this trade, or to put it more succinctly “two bites of the same cherry”.

You are borrowing funds at extremely low costs to fund investments at much higher returns.

The currency you borrowed in can actually depreciate and thus devalues your overall debt load. Supported by government policy and the net selling of the currency in question to fund the carry trade.

Over the last few decades this has been a very popular and successful investment strategy, until of course the bubble bursts – carry-trades turn around and deleverages very rapidly (pays down the debt invariably under extreme duress and pain due to a rapidly appreciating currency you actually borrowed in the first place) which in turn dries up liquidity and causes a great deflationary effect on the economies that initially benefited from this investment flow.

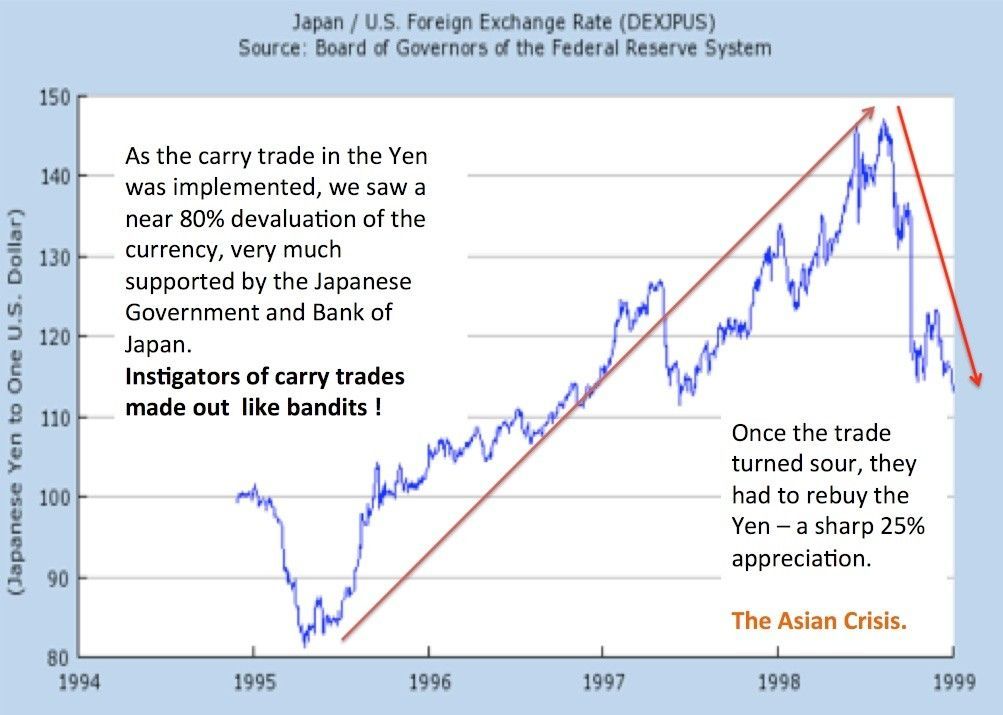

1997 – ’98 Asian Crisis

The “Yen” carry-trade was a favorite currency for the trade at that time. Hedge Funds, Institutions, domestic emerging markets (such as Thailand, Malaysia etc.) could effectively borrow money in Yen and invest in higher yielding investments elsewhere.

From 1995 into ‘98 you could borrow money at below 1% in the Yen.

This trade effectively feeds on itself and became self-fulfilling, especially with the full support of the Bank of Japan and its intention to weaken it’s currency at the time. As the trade becomes ever more popular it effectively devalues the ‘carry’ currency – as borrowers sell the Yen and purchases the currency in which they are investing into at a higher yield than the borrowing costs.

The emerging markets of Asia benefited from this huge flow of investment ‘carry-trade’ funding. The currencies of the lower-interest countries like Japan or the U.S. borrowed and invested in the much higher-yielding bonds of emerging countries. The danger of course is that when one of these countries has trouble paying the interest on its debt, there is a huge unwinding of this trade, hundreds of billions of dollars flows out, and an emerging market crisis can produce a worldwide market crash.

This deleveraging of the carry-trade simply engulfed Asia in 1997’98 as the interest payments of it’s debt doubles and even triples relative to their investment income stream in their own domestic currencies (emerging market currencies collapsed in value while the Yen appreciated 25% against the US$ alone).

Perhaps one of the most extreme episodes of carry-trade unwinding was on October 7th – 8th 1998, when the Japanese Yen abruptly appreciated 13.4% against the US dollar (target currency) in only two days after a long period of depreciation.

The emerging markets carry trade was estimated at between US$ 1 to $2 trillion (equivalent) in size.

And now….2015

Now we arrive at the great carry-trade of the moment and the largest such trade in history by a very wide margin. In fact the carry-trade of today is at least 5 times greater than the trade that effectively caused the Asian crisis.

The Bank for International Settlements in January released a report on the unstable and dizzying scale of global debt in US$.

How did this trade today become so large?

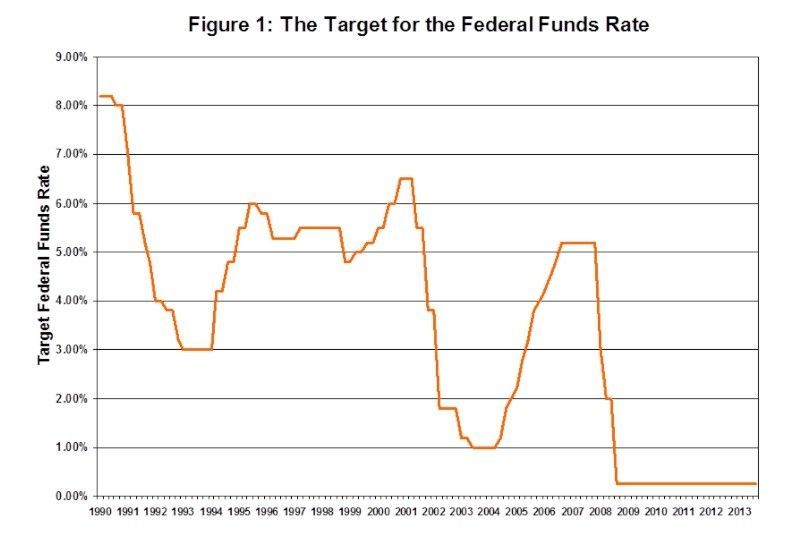

As the 2007/08 crisis hit, the epicenter of which being squarely in the USA, they reacted rapidly by lowering interest rates to near zero and literally flooded the system with fresh credit via the Federal Reserves various QE programs. This was the green light to start borrowing and funding investments in the US$ and converting that funding into other currencies.

Contrary to popular belief, the world is today more dollarized than ever before. Foreigners have borrowed $9 trillion in US currency outside American jurisdiction, and therefore without the protection of a lender-of-last-resort able to issue unlimited dollars in extremis.

Rates pushed to near zero in late 2008, along with the arrival of QE (Quantitative Easing is the new monetary policy tool, adopted by the Central Banks to increase money supply by ‘printing’ electronically money / credit into the economy by buying financial assets)

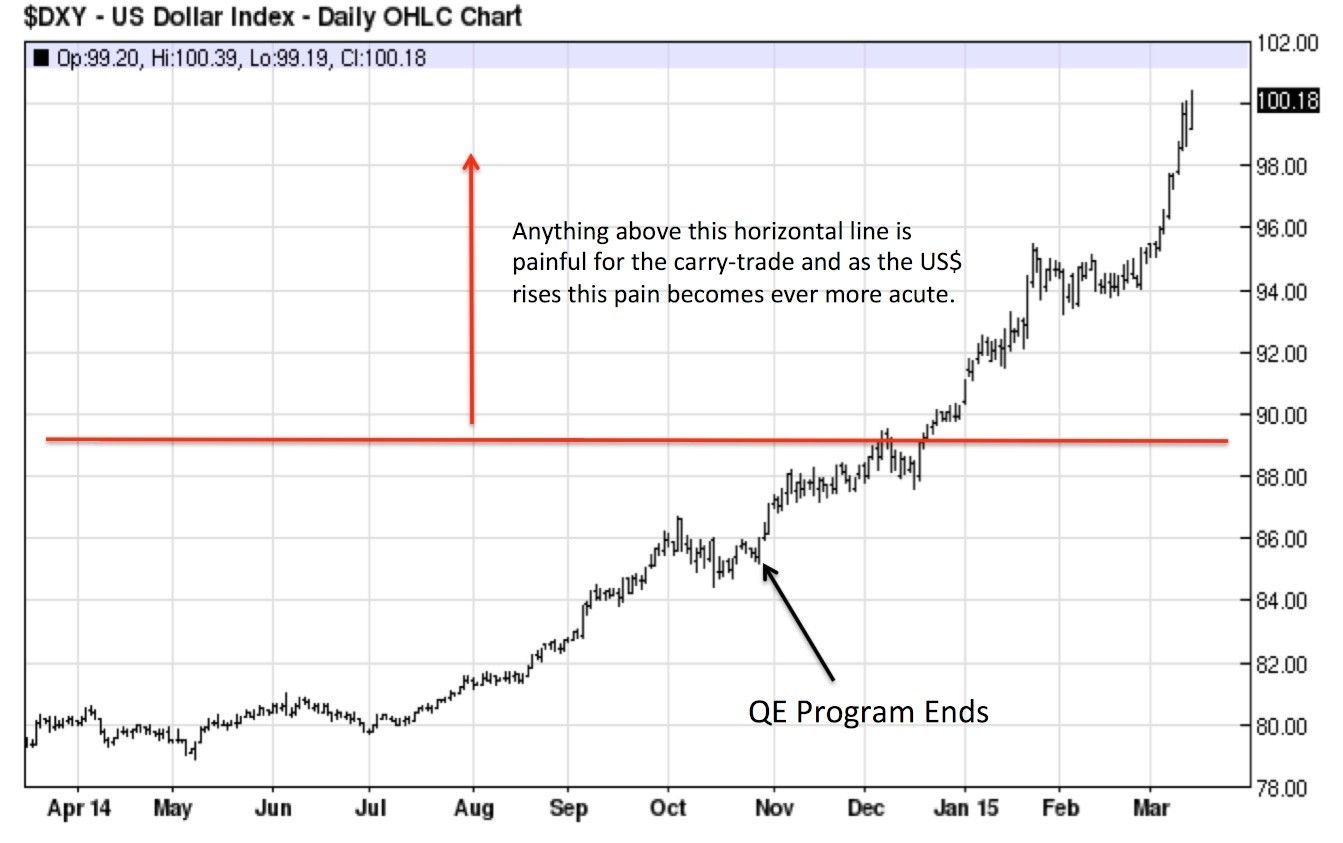

See the chart below of the US$ dollar relative to a basket of foreign currencies, know as DXY…

As you can see below, funding in US$ was also supported by money printing programs to help suppress the value of the US$.

Actually the Fed announced a tapering of the QE in December of 2013, which physically started in January.

Since then the US$ has surged approximately 25% in value, this has seriously compounded the pain in the massive carry-trade funding taken out in US$. A closer look at the US$ chart over the last 12 months below….

Companies are hanging on by their fingertips across the world. For example the Brazilian airline Gol had a very comfortable balance sheet four years ago when the Brazilian Real was the strongest currency in the world. Three quarters of its debt is in dollars.

This has now turned into a ghastly currency mismatch as the Real goes into free-fall, losing half its value against the US$ in just the last 12 months. Interest payments on Gol’s debts have doubled, relative to its income stream in Brazil. The loans must be repaid or rolled over in a far less benign world, if possible at all.

How does this end ?

If the US$ continues to rally (which it very much looks like it will do as borrowers attempt to pay down debt by purchasing US$) then this could well compound the worlds already monstrous debt loads and send the emerging markets into a tailspin which would domino effect throughout the worlds financial system.

The warning bells are ringing loudly.

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery in Singapore, Malaysia or safe storage at Free port Singapore.