Banking Crisis, Stagflation, QE, YCC

What Exactly Does This All Mean for Precious Metal Investors?

David Mitchell, 14th March 2023

I have written about the global macro-economic picture on many occasions, and while sure enough the direction has followed the path I have laid out (discounting the many black swans that have appeared, such as Covid), it seems prices of the precious metals have frustrated us all over the recent two and a half plus years consolidation pattern. Markets tend to remain irrationally mis-valued far longer than expectations or real world fundamentals.

But in this article, I will concentrate on the bigger macro picture which is more important, as I believe it will naturally take care of the metal and commodity complex price revaluations in due course.

A quick definition of the terms used in the title of this piece…

Stagflation – Persistent high inflation combined with high or growing unemployment and stagnant or contracting demand or more succinctly defined as recessionary forces in a country’s economy.

YCC – Yield Curve Control is a monetary policy action whereby a central bank purchases variable amounts of government bonds or other financial assets in order to target interest rates at a certain level. More accurately it is referred to as Yield Curve Compression, as they print money out of thin air to buy debt instruments to artificially suppress the interest rate yield curve (incredibly inflationary).

QE – Quantitative easing is a monetary policy action where a Central Bank purchases predetermined amounts of government bonds or other financial assets using currency creation out of thin air in order to stimulate economic activity. They have already instigated this past weekend their intention to backstop banks by buying securities at 100 cents on the dollar to bail out the banks’ balance sheets.

So, the Roadmap from here looks very much like this, again discounting the many black swans on the horizon:

– The Fed implement QE to backstop the banks by buying their debt securities at 100 cents on the dollar (this is already being implemented).

– The Fed will be forced to implement YCC.

– Pause/Cut interest rates.

– Currency destruction – Global Capital Flows are confirming directional shift into the commodity complex and precious metals moving to safer ground in the face of a severe crisis.

Further down in this article, I briefly cover the significant changes in global capital flows that we are starting to witness, underpinned by the rationale that…

• Following an historic 12-year bull market that set numerous records, the stock markets appear to be highly susceptible to factors such as declining corporate earnings, inventory build-ups, increased funding costs, and dire forward-looking indicators that indicate a severe recession on the horizon, beginning in 2023.

• The global property markets, having also experienced record-breaking leverage and impressive returns during a 12-year bull market, are now facing severe cracks in valuation models as a result of significantly higher funding costs and markedly weaker balance sheets.

• As interest rates have increased, the value of debt markets has experienced a significant decline, leading into the present banking crisis alongside pension fund losses to name just a couple.

Consequently, investors understanding the extreme disparities in valuation models between ‘financialised assets’ and the ‘real economy’ are beginning to shift their capital to safer ground and towards the very undervalued commodity markets and metals, with precious metals showing particularly strong potential and structure to break out from their highly favourable technical consolidation pattern over the last nearly three years.

The Sacrificial Lamb

The unequivocal fact, commonly realised at higher levels of finance is that our policy leaders, simply only have 2 choices ahead of them (which they are acutely aware of). They can either sacrifice the debt markets and allow them to implode and default on the global stage or they can sacrifice their currencies causing severe and significant purchasing power destruction. It really is as simple as that.

Historical precedence together with current policies categorically shows which side of the coin they prefer. Sacrificing their currencies will be the option they pursue, as the repercussions of sacrificing the debt markets is just too horrendous to even contemplate.

The global debt crisis is starting to blow up, so I will try to explain how these developments are manifesting and what exactly they mean for all of us…

Debt Markets

I have written over the last 12 months across a number of articles that effectively the 10-year US Treasury debt market (I concentrate on the US markets as they are leading the world’s debt markets) cannot rise above 3.5% to 4% (as a rough estimation) in yield, otherwise the repercussions would be overwhelming. In fact, in October 2022 we got close to 4.25% which funny enough aligned itself with the Bank of England having to instigate a mass bailout of the UK Pension Funds via the instigation of YCC (Yield Curve Control) to the tune of £65 billion. Presently the USA 10-Year is trading at 3.70% on the back of the new US Banking crisis that has suddenly appeared as of last week culminating on Friday 10th March, 2023.

Let us not beat about the bush here, the Federal Reserve of the USA through cause and effect have been a part of, or outright caused, every economic crisis of the last 40 years, progressively making larger missteps using faulty Keynesian models and completely ignoring the Quantity Theory of Money, to keep the train on the tracks. They created (with the help of governments) the inflation monster in the first place (I will not go over that ground again as I have covered this in previous articles) and now they have simply taken it too far in the opposite direction with the fastest tightening (interest rate increases) in history, alongside a negative contraction in the money supply while we are all sitting on the largest global debt crisis in history.

The Federal Reserve will tighten until something breaks… Well, they have now broken two banks, with Silicon Valley Bank (SVB) becoming the second largest bank failure in U.S. history and Signature Bank which is a major New York bank.

So, before I give a clear picture of how this is going to pan out and what we need to expect, let us dispel the present and ludicrous rhetoric of a soft economic landing versus the reality of the hard landing / deep recession that the data is clearly pointing to.

Recession Delayed, But It Is Still Coming

Now let me be clear here, employment data is a wholly lagging indicator, as companies only lay off staff as their companies turn down, so taking comfort that employment is high and hence the economy is healthy is nonsense as a forward barometer.

The notion that we are on the cusp of a new era of economic prosperity, characterized by a new resurgent stock market and a rebounding job market fuelled by China’s emergence from lockdown, is a fallacy that must also be dispelled. The current prevailing sentiment, that we have successfully avoided an economic recession and are now poised for sustained growth, is misguided. The reality is that, based on historical economic indicators, Europe and the US are hurtling towards a dire economic downturn. It is akin to driving a car at full speed towards a wall, with the accelerator pedal pressed down and expecting a positive outcome!

Firstly, let us look at OECD’s composite leading indicator for the G20 nations that has been in a consistent state of decline for the past 17 months, with no indication of stabilizing. January saw the index plummet to a new low of 98.4, which strongly suggests that the economy is heading towards a recession.

The major G7 countries are in an even more precarious state, with their readings plummeting to 98.1. This figure is the lowest it has been since the dotcom recession of the early 2000s. Italy is facing particularly challenging economic conditions, as its current state is recorded in January at 96.70, in fact lower than during the eurozone debt crisis a decade ago. The UK is even more dire at 94.50 and facing a grim economic outlook.

In another sign, Capital Economics said its global trade monitor had yet to detect any sign that global shipments have touched bottom. “Not only did the fourth quarter see one of the biggest drops in world goods trade since the 1980s, but leading indicators point to further falls ahead,” it said.

The USA Dallas Federal Reserve has done a new survey stating the price-to-income ratio has hit levels never seen before in modern US history. They think house prices could fall 20% in the US, with parallel falls in Germany, risking a “domino effect” through the global macro-economy. US house prices peaked last June and have since fallen by 4.4%. This is only the second time since the 1930’ that US house prices have fallen nationally.

The US Federal Reserve and the European Central Bank are implementing the most forceful monetary tightening measures ever seen in history, despite the fact that sovereign, public, and private debt ratios have skyrocketed to unprecedented heights.

Companies have taken advantage of low or zero interest rates over the preceding 2 to 3 years by stretching out their debt maturities to create a temporary safety net. However, the harsh effects of this intense tightening have yet to take full effect, and there are already indications of an emerging credit crunch in Europe.

S&P Global says that US firms have a weaker credit profile than before the Lehman crisis. “Refinancing pressure is building,” it said.

Deficits in a Recession

As countries move into economic contraction, actual debt loads explode in size, as economies garner less taxable income from contracting earnings, but also as a record number of employed start to lose their jobs en masse, the social safety net has to expand to support the populace in times of distress.

For example…

The US deficit spending in 2022 was US$1.4 trillion (5.5 percent of GDP) and is expected to rise (based on a growing economy) to US$1.6 trillion (6.0 percent of GDP) in 2023. However, using forward analysis based on past historical recessions and their effects on deficits, the guidance is that the yearly US government deficits are likely to explode to between US$3 to US$3.5 trillion per annum over a recession, i.e. 2023 into 2024? – Exactly who will be purchasing the tsunami of all this new debt issuance?

Yield Curve Compression

Within this environment and the momentum of the deterioration within the debt markets the USA is going to be forced into artificially suppressing interest rates over the yield curve via official policy. By taking that step, it will become evident to everyone that the debt markets are being prioritized over the currency markets, resulting in a severe loss of purchasing power for the currency, commonly known as inflation or financial repression.

In the 1970s inflation came in 3 waves, each one being metrics larger than the previous one. We seem fully destined to face exactly the same fate. Inflation is falling presently (present 2nd wave of inflation) with the fierce monetary tightening and contraction of money supply, but the 3rd wave higher in inflation will arrive as sure as night follows day.

Unrealistic Stock Market Expectations?

From any valuation metric perspective we wish to look at, the US market in particular, is very overvalued indeed historically. That said, we have an overriding destruction of currency value on its way, and so this must be taken into consideration from a porfolio persepctive.

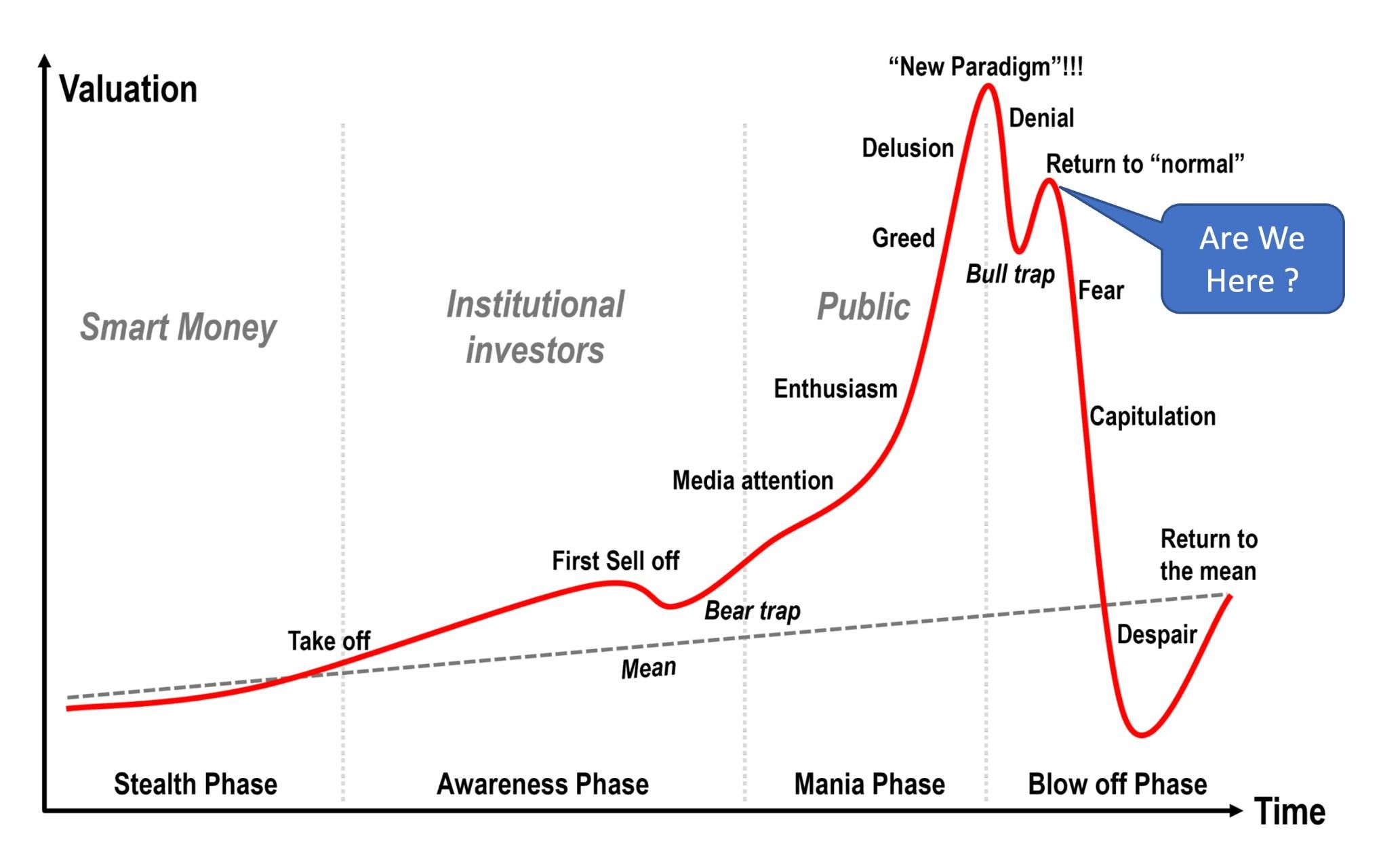

In view of the technical price charts, macro fundamentals, contracting corporate earnings, recessionary forward indicators, dramatically rising geo-political tensions and unsustainable debt dynamics to name just a few, I would strongly suggest we are in the upper right of this chart, the “Return to Normal” perspective.

Now the outlier or deviation in my thought process and the longer term valuation models, is that of course we face a 3rd wave higher in inflation (serious currency value destruction) and hence capital will seek to stay within the stocks markets, hence in nominal US$ terms, the stock markets (discounting high price volatility) will likely stay around these levels moving forwards, but in “real” US$ terms, investors will experience significant loss of purchasing power as the competing asset classes such as precious metals and commodities will significantly rise in value.

Now the outlier or deviation in my thought process and the longer term valuation models, is that of course we face a 3rd wave higher in inflation (serious currency value destruction) and hence capital will seek to stay within the stocks markets, hence in nominal US$ terms, the stock markets (discounting high price volatility) will likely stay around these levels moving forwards, but in “real” US$ terms, investors will experience significant loss of purchasing power as the competing asset classes such as precious metals and commodities will significantly rise in value.

Global Capital Flows Into the Real Economy, 120 Years of History – Commodities & Metals

Our central banks and governments will attempt to move heaven and earth to support their economies, and hence we face a significant forward guidance of Stagflation, which is economic stagnation on the back of decades worth of overextension and artificial valuations based on debt leverage alongside severe currency value destruction (inflation). This will occur as they throw money at the economy and expand deficits, while significant shortages and tightness within the commodity complex forces global capital flow to move to higher ground.

In fact, going back through history, particularly the last 120 plus years since 1900, we have experienced three previous events in the 1930s, 1970s and 2000s, where global capital flow shifted and moved out of “Financialised Assets” including Bonds, Equities and Property and into the “Real Economy” comprising Precious Metals, Commodities and Infrastructure. During these three previous periods of shifts in global capital flows, we saw a significant loss of value in “Financialised Assets” while the “Real Economy” saw exponential revaluations higher.

We are seeing first-hand the developments of de-globalisation, rising global geo-political tensions, currency destruction and imploding debt markets, weak governments, social unrest and loss of faith in our central policy markets and central banks.

Historically this has proven to have been a very rich and fertile breeding ground for explosive moves higher in precious metals, will this time be any different? I don’t think so!

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery across the world.

Consider the safest option of segregated, allocated vault storage at Le Freeport Singapore with Indigo Precious Metals.

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.