“QE Benefits Mostly The Wealthy” JPMorgan Admits, And Lists 8 Ways ECB’s QE Will Hurt Everyone Else

Originally posted on zerohedge

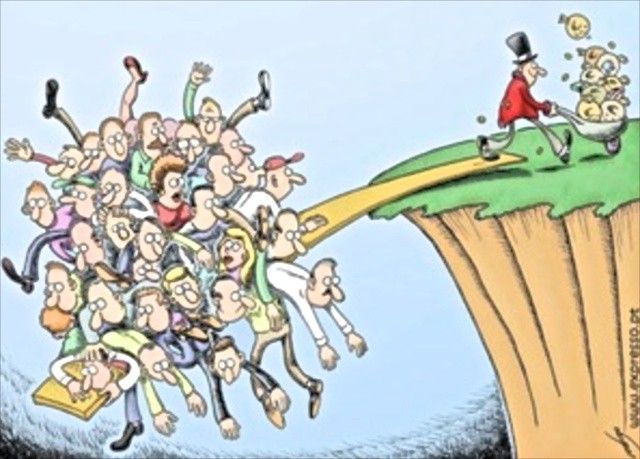

JPMorgan’s Nikolaos Panigirtzoglou, who recently said what has been painfully clear to all but the 99% ever since the start of QE, namely this: “The wealth effects that come with QE are not evenly distributing. The boost in equity and housing wealth is mostly benefiting their major owners, i.e. the wealthy.”

Thank you JPM.

And of course, even the benefits to those who stand to gain the most from QE are only temporary. Because the same asset prices which rise thanks to money printing are only transitory, and ultimately mean reverting. To wit: “It potentially creates asset bubbles by lowering asset yields by so much relative to historical norms, that an eventual return to normality will be accompanied with sharp price declines.”

As for everyone else, here is a list of 8 ways that the ECB’s QE will hurt, not help, by way of JP Morgan.

* * *

1) Lower bond yields can increase pension fund and insurance company deficits reminding pension funds of the need to match assets and liabilities. We highlighted last week how record low bond yields caused a sharp widening of pension fund deficits, with UK pension fund deficits in particular rising back to May 2012 record highs. In regions where regulatory restrictions are higher, like in Europe, larger deficits induce pension funds and insurance companies to move further away from equities and other high risk assets into fixed income. Because of these regulatory restrictions, we think it is fair to expect that the large wealth effects we saw previously with the Fed’s QE will not be repeated in the euro area with the ECB’s QE.

2) QE is creating a regime of low bond yields but also higher uncertainty. At the least, QE makes central bank exit more difficult and raises the risk of a policy error or of an increase in perceptions about debt monetization. It potentially creates asset bubbles by lowering asset yields by so much relative to historical norms, that an eventual return to normality will be accompanied with sharp price declines. Perceptions about asset bubbles can thus also increase long term uncertainty. In turn higher uncertainty might prevent economic agents such as businesses from spending.

3) Ultra low credit spreads and corporate bond yields are an intended consequence of QE but not without distortions. By potentially allowing unproductive and inefficient companies to survive, helped by ultra low debt servicing costs, QE can hinder the creative destruction happening during a normal economic cycle. To this extent, QE can make economies less efficient or productive over time.

4) The wealth effects that come with QE are not evenly distributing. The boost in equity and housing wealth is mostly benefiting their major owners, i.e. the wealthy. Savers, who are long cash, are instead suffering an erosion of their income and wealth. In the case of euro area more specifically, given structurally lower allocation to equities by households, any potential boost to equity prices from the ECB’s QE will likely have smaller wealth and confidence effects than the Fed’s QE had in the US.

5) QE can exacerbate so called “currency wars”. From a policy point of view, Denmark’s central bank decision this week to take its deposit rate deeper into negative territory to -0.30%, and the SNB’s decision last week to abandon the defense of its minimum exchange rate vs. the euro and to lower its depo rate to -0.75%, shows how difficult it is becoming for neighboring countries to follow the ECB’s shift towards even easier monetary policy. But the ECB does not pose a challenge only for its closest neighbors. Euro area’s main competitors across EM and DM will feel the pressure from a sharply weaker euro inducing them to ease or tighten by less. In EM, currency wars typically result in FX intervention and accumulation of foreign currency reserves or capital controls in more extreme cases, pushing back DM bond investors back to their own markets.

6) QE hurts banks. Commercial banks are facing the risk of shrinking interest rate margins and profitability as there is little room to lower deposit rates, which are close to zero, as lending rates collapse. The experience from Denmark, which was the first country to introduce a negative depo rate in July 2012, showed that banks did suffer an erosion of their profit margins as lending rates declined faster than deposit rates. Admittedly lower interest rate margins do not appear to have hurt credit creation in the case of Denmark over the past two years, so the hope is this side effect will be confined to the banking sector and not hinder credit creation in the euro area economy.

7) But it is not only commercial banks that are hurt. Reduced turnover and liquidity has hurt the fixed income trading across investment banks in recent years and the ECB will likely exacerbate recent trends. We argued before how UST collateral shortage has hampered US repo markets “Reverse repos do little to alleviate UST collateral shortage”, July 11th 2014. The ECB looks set to inflict similar damage to European repo markets as government collateral will be withdrawn at a pace of close to €45bn per month from March onwards. We think an argument can be made that the damage to trading turnover and liquidity is likely to be even bigger with the ECB’s QE relative to the Fed’s QE, because the ECB went even further than the Fed by lowering its policy rate to negative territory. Naturally negative yields hamper trading volumes and liquidity as market participants are less willing to trade at negative yields.

The ECB’s deposit rate cut to negative in June brought both secured and unsecured overnight rates to negative territory. In repo markets, overnight general collateral secured rates have exhibited high volatility hovering between -15bp and zero over the past six months, meaning that investors looking to cover short positions have to lend cash at negative rates. Negative nominal rates are also prevalent in short-dated government bonds. But what is becoming more of an issue is that longer-dated euro government debt, i.e. debt with longer than 1-year maturity, is increasingly trading with negative yields. Figure 1 shows an estimate of the amount of Euro area government bonds with longer than 1-year maturity trading at negative yields over time. We use pricing data from our JPM bond indices. On this estimate, around €1.4tr of Euro area government bonds are currently trading with negative nominal yields, almost all of them of core euro governments of up to 5 years maturity. Back in June, before the ECB’s shift to negative depo rate, the amount of euro area government bonds with longer than 1-year maturity trading negative was virtually zero.

8) QE creates political frictions which could escalate in the future once QE becomes a negative carry trade for central banks, i.e. when the interest on excess reserves starts rising above the yield they receive on their bond holdings. These political issues could reduce the coordination between government and central bank policy or even jeopardize central bank independence in the future. Political issues are even bigger in the euro area because of its fragmented status. Within the euro area, political differences between inner core countries such as Germany and the rest intensified as a result of this week’s QE announcement, and this could jeopardize the process of much needed fiscal and political integration in the future. The decision by the ECB to subject only 20% of the new bond purchases to risk sharing across the Eurosystem shows the compromises that the ECB has to make already in light of political differences. This is not to say that that the 20% limit on risk sharing will affect the effectiveness of the QE program. Neither will it protect Germany in the future against a sovereign default by another country, in our view. After all, if markets start doubting the debt sustainability of a country, the Target2 balances will widen, causing an exponential rise in Bundesbank’s exposure to the rest of the euro area, irrespective of the degree of risk sharing in ECB’s QE. It is more about the doubts that this risk sharing decision raises regarding political commitment to the euro project.