2022 in Short Review, What to Expect in 2023,

Explosive Moves Higher in Metals?

David Mitchell, 8th January 2023

I wish you all a wonderful New Year, with happiness and health always the main focus. And Gong Xi Fa Cai, to all of our Chinese friends and clients. 2022 was the Year of the Water Tiger, a turbulent year with tense geo-politics and global asset market valuation drubbings, but it was not a global crisis year per se. The Year of the Rabbit in 2023 will deliver an entirely different year compared to last.

As I have written about for many years, from a long-term cycles perspective, 2023 was destined to be a “Crisis Year” leading into a dangerous 2024. By examining the global macroeconomic landscape presently it very much looks like cycles are yet again going to prove their ability to accurately predict.

Reflecting on the past year is always healthy from the perspective of recognising our macro-forecasts and to ascertain that developments are indeed moving in the direction that we perceived to be correct. Understanding what this means moving forward is equally important. Any analyst, trader and wealth manager has a mandate to re-evaluate their macro and technical pictures constantly and I personally take that very seriously. As markets, politics, geo-politics and black swans develop you do need to reassess your asset portfolio weightings.

No one has a magic predictive crystal ball, but cycle analysis overlaid with technical chart scrutiny, global capital flow analysis and fundamental macro examination is the closest you will get to a glass ball in the investment world.

I wrote an article in January 2022 ‘Awakening The Tiger‘ and it is well worth reading the article again, as it set-out the picture of how 2022 would develop, and ultimately the outlook for the next few years.

The past year has been anything but ordinary, but in retrospect, it was very much expected and forecasted in our bigger picture analysis. It was a very bruising year for the mainstay majority investor indeed, in fact the overriding typical portfolio having a 60/40 mix, combining 60% across the stock markets and 40% in debt instruments, has had the worst year since 2008 and the second-worst performance on record since 1976. 2022 suffered the intimidating combination of war, extreme inflation, energy scarcity, global political mis-management, rising global de-carbonisation policies, insane global aggregate contraction of money supply (fastest contraction in modern history and squarely led by the USA’s Federal Reserve), disastrous Covid lockdown of China’s economy, the bursting of the crypto and NFT bubbles, and the list goes on and on.

What occurred in 2022 was most definitely not the consensus view over 12 months ago. The vast majority expected life was just beginning to progress forward again following on from the COVID-19 pandemic. Investors cannot continue to misstep at this stage (in 2023) as that would be naïve. We have still yet to pay the ‘Pied Piper’ (being the global debt disaster), at a time when there has been a truly historical misallocation of capital, which has developed over the last 10+ years in particular.

I will be focused on writing several reports in January covering 5 different directions; subjects I spend a great deal of time studying and all of them I believe to be very important moving forwards. I will analyse them individually, so as to keep this article short and sweet.

What to expect in 2023?

Over the last 12 years investment capital flow has concentrated very heavily into the financialised economy, with the advent of free zero-cost capital (no longer the case), strongly invigorating capital moves into the ‘financial economy’. This was accompanied by mass speculative positioning and leverage into stocks (technology stocks in particular), housing and cryptocurrencies, to name just a few. This wholeheartedly crowded out CapEx investment into the ‘real economy’ (commodity production, infrastructure to support the commodity complex, equipment investment etc), as the opportunities for global “casino” speculation and leverage alongside all of the newly created cash (monetary aggregate expansion, i.e. money printing) was way too seductive to resist. This capital flow soaked up the majority of the investment capital away from the commodity complex (the production of commodities) thus creating mass valuation bubbles.

CapEx within the ‘real economy’ (the hard production of commodities) is running well below inflation and in ‘real terms’ has grown zero percent over the last 10 plus years, even though the global economy itself (and global population) has expanded dramatically in size.

Investment and infrastructure build-outs into a solid future proof energy base load, green transformation investment, food production and rare metal production (to name but a few) across the whole commodity base has simply been woeful. This is now driving severe shortages and extraordinary infrastructure problems across the entire commodity complex. Hence another great capital flow shift is in its infancy but is most assuredly underway. We refer to this as the “4th Great Turning” (one of my 5 subject articles to come, that I have been analysing in great detail over the last 6 months).

I strongly suggest that twenty plus years from now, this will be seen as the necessary ‘great’ forest fire in financialised asset valuations, required to force capital into the ‘real economy’ leading us back into an age of bountiful productive economic gains based on a huge real economy investment flow build-out. However, the stagflationary debt crisis that we have to endure first, will be enormously painful for the vast majority of investment portfolios and people’s present perception of their own wealth.

These dramatic problems across the commodity sectors have been temporarily hidden from us in 2022, driven by two significant events. Firstly, Western Central Banks, led by the Fed in the USA have driven interest rates dramatically higher, while at the same time contracting the money supply at the fastest rate in history. This policy is publicly labelled as outright ‘demand destruction’.

Secondly, China, the 2nd largest economy in the world, continued to completely lockdown their economy due to Covid. China is now opening up and the pent-up demand built up over 1,000 days of total lockdown is about to put incredible demand pressures on real stuff. The global interest rate increases only look to one side of the scales (namely temporary demand destruction) whilst ignoring the most important side of the inflationary coin, namely supply!

Inflation is not going away (we are undergoing a monetary debasement), in fact there will be another major wave higher in the years ahead (I expect higher highs measured in inflation metrics). The Central Banks at that point will be under considerable pressure from severely weakening economies due to rising cost of capital, debt markets imploding and the repercussions thereof, and the fall-out from the global debt crisis, along with balance sheets negatively affected by contracting margins due to the impact of high inflation.

Sentiment Cycles Within The Greater Asset Class Cycles

It is important not to let your emotions get in the way of making smart investment decisions. Within a protected asset portfolio, one must understand the level of diversification required and maintain a clear understanding of the macroeconomic and geopolitical situations and major cycle capital flow analysis moving forwards. With this approach, you can then be better placed to fully grasp why precious metals in particular offer such an exceptionally attractive investment thesis; especially from this juncture onwards.

It is then important to determine how such a portfolio of precious metals should be optimally weighted at this stage. It is notoriously difficult to separate emotion from the realities of market action and price overextensions (either up or down) and this tends to lead to unchecked emotional decisions, giving rise to suboptimal investment choices.

We expect precious metals to have another volatile year ahead because of the ongoing and severe economic and geo-political headwinds. The data we analyse alongside the cycles and technical pictures, side-by-side with incredible supply-demand deficit pressures that continue to develop, we are forecasting explosive rallies to materialise within the precious metals in 2023 and into mid 2024.

Auctus Metal Portfolios, Offering Active Portfolio Management, Outperformed in 2022.

Our models analyse an enormous amount of metals data on a daily basis, with the sole mandate for maintaining optimal portfolio weightings based on present market prices. Auctus Metal Portfolios’ models do not trade the market, they are however, constantly looking at trends and momentum analysis to maximise the gains for our clients over and above a static holding of metals.

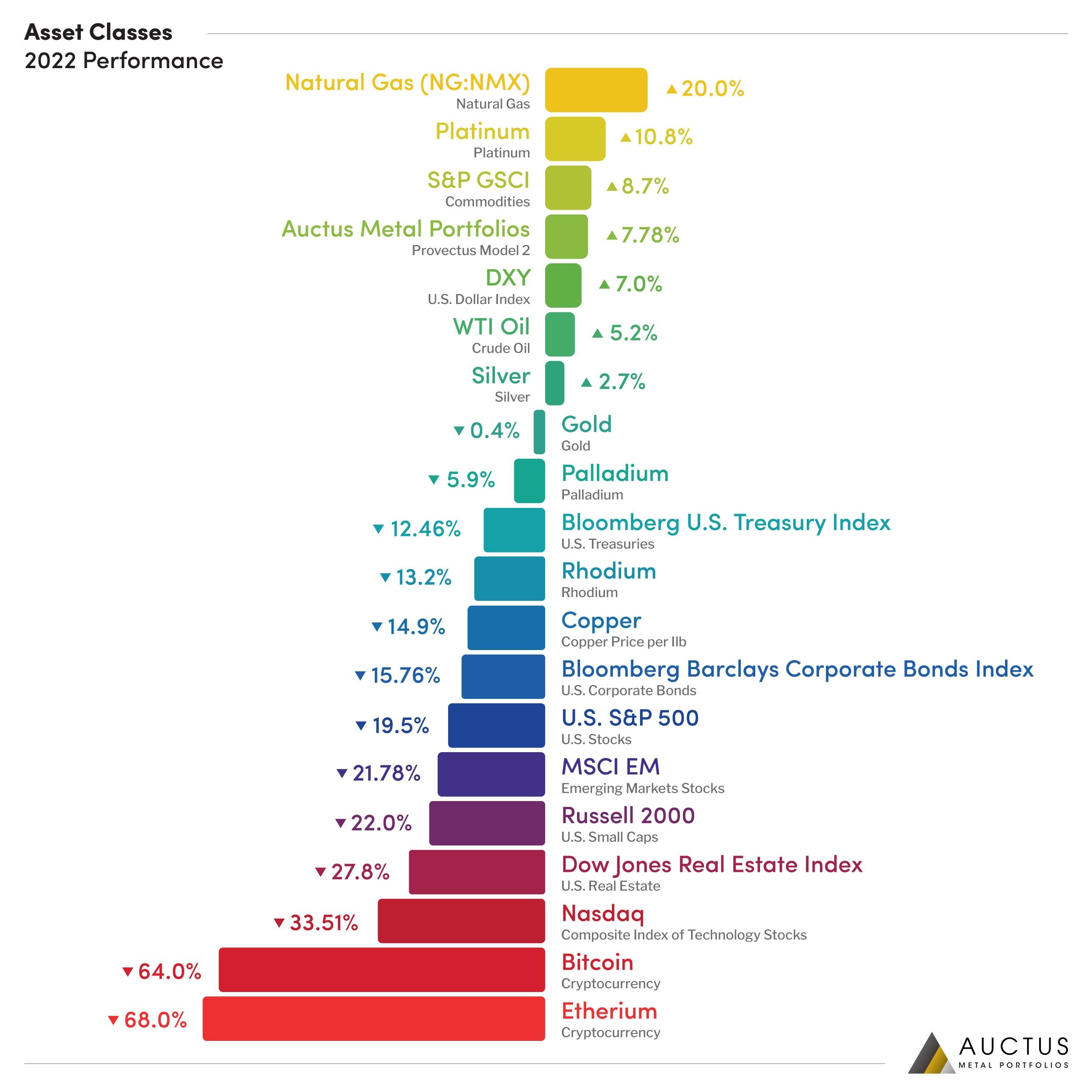

The last 12 months have been incredibly quiet in terms of re-balancing Auctus clients’ physical precious metal portfolios. That said, the portfolios remain very overweight in Platinum with a smaller percentage in Silver. With Platinum being the outright winner in 2022 with a calendar year performance of +10.8% versus the US$ and Silver coming in at +2.7% the models have again successfully proven their worth.

Gold was mostly flat for the year and finished at -0.4%, Palladium was -5.9% and Rhodium -13.2%, none of which were in our Auctus client’s portfolios in 2022.

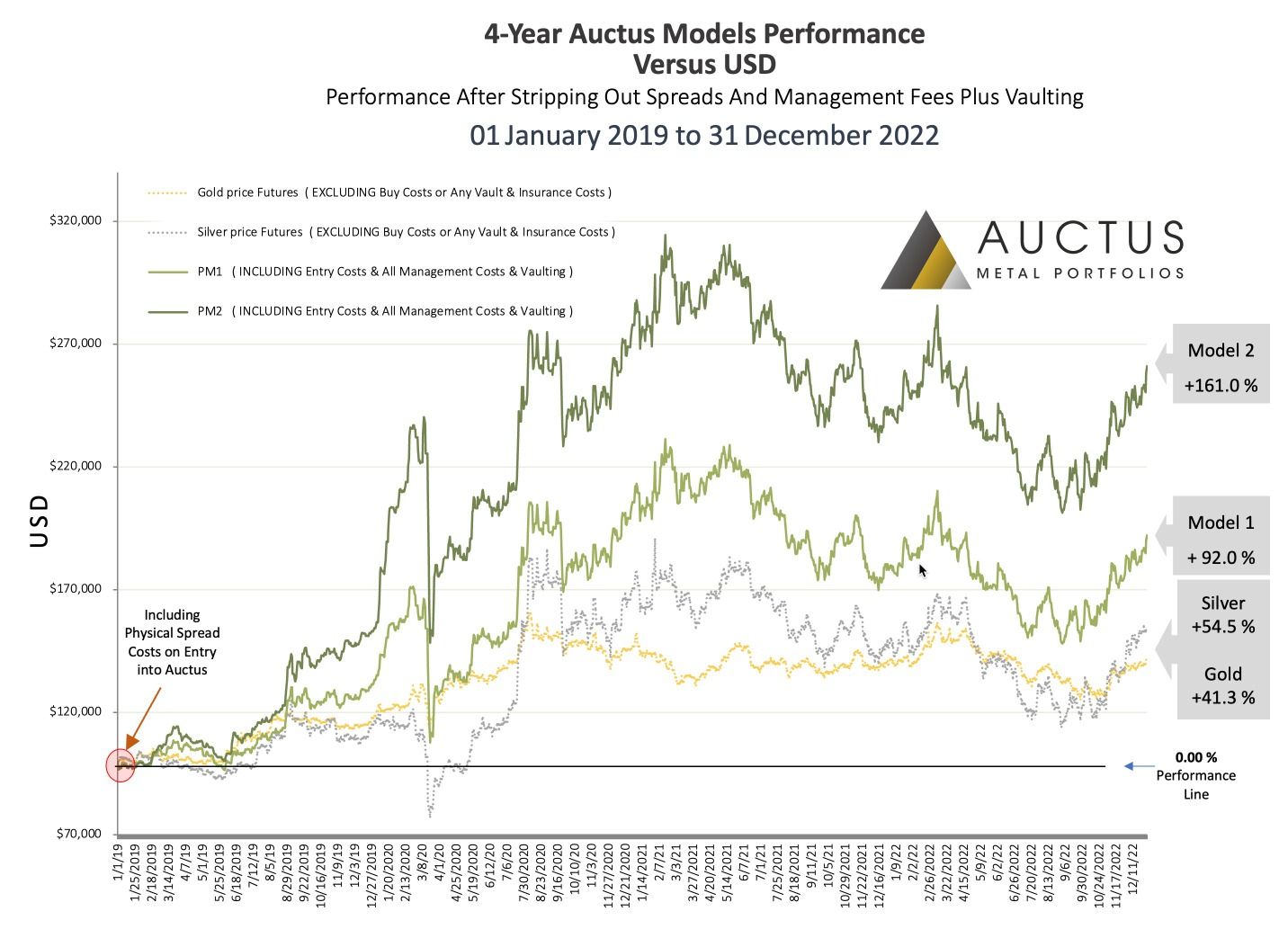

Auctus Metal Portfolios’ (Provectus Model 2) Net Return on Investment

to 31 December 2022

After Spreads, Management Fees and Vaulting Costs are Deducted

Calendar Year Performance | Net Return to Clients

7-Years: +833.54% since 1 Jan, 2016

5-Years: +212.55% since 1 Jan, 2018

3-Years: +40.63% since 1 Jan, 2020

1-Year: +4.53% since 1 Jan, 2022

Please note that the net returns above have been calculated after all transaction costs have been stripped out, this includes (bid / offer spreads), vaulting fees and also Auctus Metal Portfolios’ management fees. Zero leverage or collateralization is applied to any clients vaulted holdings.

Disclaimer: These returns take into account funds that have been fully invested from 1st January calendar year stated, and do not take into account client performances when entering at different time frames within the stated overall performance ranges.

Wishing you all a wonderful year ahead.

David J Mitchell

CLICK HERE to download the full report

Protect your wealth; invest in physical gold, silver or other precious metals at best prices from Indigo Precious Metals. Physical delivery across the world.

Consider the safest option of segregated, allocated vault storage at Le Freeport Singapore with Indigo Precious Metals.

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.